2024/40 “Just Energy Transition Partnerships (JETPs) in Indonesia and Vietnam: Implications for Southeast Asia” by Melinda Martinus

EXECUTIVE SUMMARY

- JETPs emerged during COP26 as a significant multilateral climate financing initiative undertaken by the International Partners Group (IPG) to assist developing countries like South Africa, Indonesia, Vietnam, and Senegal in transitioning away from coal.

- JETP implementation in Vietnam and Indonesia faces challenges such as significant financing gaps, criticisms regarding the attractiveness of financing packages, difficulties in aligning donor and recipient countries’ expectations, the complex political-economic landscape of the coal industry, and concerns over the social impacts of energy transitions.

- Indonesia requires a staggering US$66.9 billion to fund over 400 priority projects aimed at achieving its power sector transition pathway goals by 2030. Despite receiving US$20 billion JETP funding, Indonesia still faces a substantial 70% financing gap.

- Vietnam needs US$135 billion to overhaul its electricity sector, including stopping the issuance of permits for new coal plants, building new renewable power plants, and upgrading its electricity grids. Despite the infusion of US$15.5 billion of JETP funds, Vietnam confronts a towering 89% financing gap.

- Despite challenges, JETPs offer momentum for Indonesia, Vietnam, and the region to accelerate their energy transition and unlock inclusive development. JETPs can serve as catalysts for energy transformation, allowing both countries to experiment with different financial strategies and to strengthen governance structures for effective energy transition.

* Melinda Martinus is the Lead Researcher in Socio-cultural Affairs at the ASEAN Studies Centre, ISEAS – Yusof Ishak Institute.

ISEAS Perspective 2024/40, 4 June 2024

INTRODUCTION

The annual United Nations Climate Change Conferences (COPs) have become important forums for global countries to establish common targets for reducing the impacts of climate change. However, many concrete actions extend beyond COPs. For instance, Just Energy Transition Partnerships (or JETPs) are initiatives that emerged during COP26 in Glasgow. JETPs serve as the first multilateral climate financing initiative targeting energy transition supported by the International Partners Group (IPG), primarily composed of G7 countries. To date, four developing countries, South Africa, Indonesia, Vietnam, and Senegal, have committed to JETPs, with a combined financial assistance totalling US$46.6 billion.

JETPs stand out for several key reasons. First, they prioritise assisting developing countries in transitioning away from coal, given that coal-fired electricity generation is the main contributor to carbon emissions in the power sector. Second, these partnerships facilitate the involvement of private sector funds to address gaps in climate financing. Third, while financial institutions drive the investment, JETPs emphasise that receiving countries take the lead in the implementation. This ensures that initiatives are tailored to local contexts and priorities. Finally, JETPs underscore the importance of a “just transition”, whereby green transformation should avoid negative impacts on specific groups of people.

The JETP financing mechanism is massive in scale, even compared to other more mature multilateral funds for climate change, such as the Green Climate Fund (GCF), the Global Environment Facility (GEF), or REDD+ (Table 1). For instance, the GCF, often considered the most prominent climate financing institution for mitigation with worldwide operations, has only disbursed US$13.5 billion (excluding co-financing) since its inception in 2015.[1] Meanwhile, the GEF, a biodiversity-targeted fund, has disbursed US$30 billion since the 1990s.[2] The REDD+, a voluntary climate change mitigation framework for reducing emissions from deforestation in developing countries, provided US$5.6 billion since 2008.[3] In contrast, JETPs have promised a total package of US$46.5 billion to date solely to four countries. However, JETPs alone might not be sufficient to assist recipient countries in transitioning to renewable energy sources entirely due to significant financing gaps, different expectations and implementation standards from donor and recipient countries, the complex political-economic landscape of the coal industry in recipient countries, and concerns over the social impacts of energy transition.

Table 1 Multilateral Financing for Tackling Climate Change

| Initiative | Year | Total Pledged*/Disbursed US$ | Focus |

| Just Energy Transition Partnerships (JETPs) | 2023-now | 46.5 billion* | Energy transition |

| Green Climate Fund (GCF) | 2015-now | 13.5 billion | Climate mitigation |

| Global Environment Facility (GEF) | 1990s-now | 30 billion | Biodiversity conservation |

| Reducing Emissions from Deforestation and Forest Degradation in Developing Countries (REDD+) | 2008-now | 5.6 billion | Forest conservation |

Source: author’s compilation

OVERVIEW OF JETPS

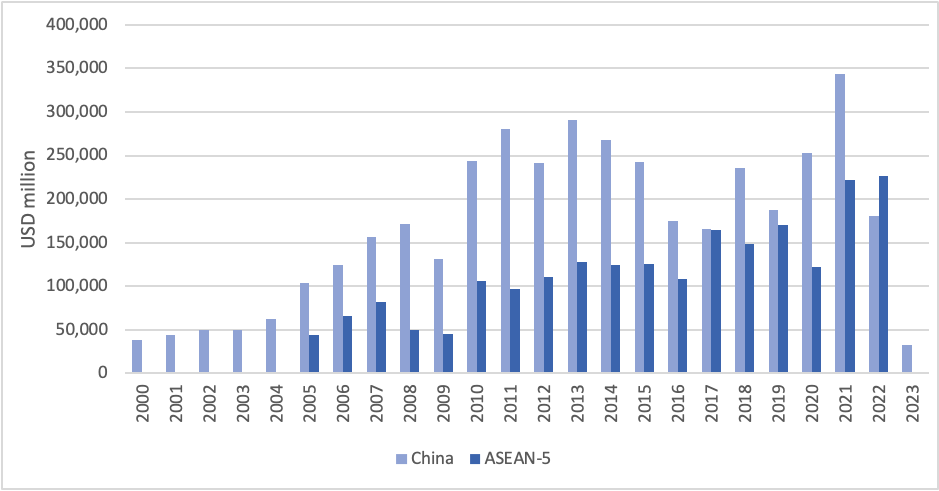

Table 2 presents an overview of JETP roll-outs in four countries. JETPs in these countries will be implemented within a three to five-year timeframe. The composition of donor or IPG countries varies slightly among recipient countries but generally includes major powers such as the UK, the US, and the EU. Interestingly, compared to their African counterparts, the two Southeast Asian countries, Indonesia and Vietnam, have attracted a more diverse array of partners, including Japan, Norway, France, Germany, Italy, and Denmark. The wide range of partners indicates that the energy transition in these two countries is much more attractive for investment. Strategically, a wide range of partners will also bring much more diverse foreign investments to balance China’s dominance in renewable energy investment in the region.[4]

The total assistance provided to recipient countries also varies significantly, with figures ranging from US$2.5 billion for Senegal, US$8.5 billion for South Africa, US$15.5 billion for Vietnam, and US$20 billion for Indonesia – corresponding to the size of each country’s market for the energy transition.

Table 2 JETP Roll-Outs in Receiving Countries

| South Africa (2021) | Indonesia (2022) | Vietnam (2022) | Senegal (2023) | |

| Timeframe | 2023-2027 | 3-5 years | 3-5 years | 3-5 years (from 2023) |

| International Partners Group (IPG) Composition | UK, US, France, Germany, and EU | Japan, US, Canada, Denmark, EU, France, Germany, Italy, Norway, UK | EU, UK, US, Japan, Germany, France, Italy, Canada, Denmark, Norway | France, Germany, UK, Canada, EU |

| Total Assistance | US$ 8.5 billion | US$ 20 billion (10 by IPG and 10 by GFANZ ) | US$ 15.5 billion (7.75 by IPG and 7.75 by GFANZ) | US$ 2.5 billion and potentially enlarged in the future |

| Policy Design | – New quality jobs in renewable energy – Development of new sectors (EV, hydrogen) -Address energy security | – Increase energy efficiency and renewables – Value chain enhancement: downstream of critical industries for energy transition (e.g., solar cell manufacture) | – Improve transmission grid capacity and storage – Development of offshore wind power – Deployment of ‘transition’ technology such as carbon capture and co-firing with ammonia | – Resilience strategy in the energy sector – Transitioning from highly polluting fuels to clean energy (via gas) |

| Target and Regulatory Approach | – Establish a 66 GW pipeline of renewable energy project – Speed up the Electricity Regulation Act Amendment Bill | – Cap emissions from electricity generation at 250 MtCO2 by 2030, down from a previous target of 290 MtCO2 – Stop building new coal-fired power plants after 2023 (exclusion for coal-fired power plants on the pipeline and captive plants) | – Reduce peak capacity of coal-fired power plants to 30.3 GW by 2030, down from the previous 37 GW plan – Speed up the Direct Power Purchase Agreement (DPPA) regulation | – Increase the share of electricity generated by renewable energy to 40% by 2030 |

Source: Adapted from UNRISD’s Just Energy Transition Partnerships (JETPs): What Do We Need to Know to Assess Them? and various sources

Each recipient country defines their own transition policy. In the two African countries, the emphasis on energy security is stronger due to the significant challenge of supplying people with reliable electricity access. South Africa currently faces challenges from a series of rolling blackouts. Eskom, the government-owned enterprise that dominates the energy sector, operates 14 coal-fired power plants, accounting for approximately 80% of the nation’s electricity generation. Many of these facilities are outdated, inefficient, and susceptible to frequent malfunctions. The construction of two more modern coal-fired power plants, initiated in 2007, has been beset by budget overruns and design deficiencies, resulting in their failure to operate at full capacity.[5] Unlike its JETP counterparts, Senegal’s current fossil fuel fleet is dependent on imported fossil fuels instead of coal, and the coal industry is not a comparatively large employer compared to the coal industry in other JETP countries.[6] Senegal, meanwhile, has a major natural gas reserve and is poised to be a major gas producer. Therefore, the JETP plan in Senegal emphasises the importance of bypassing coal and transitioning to temporary, yet cleaner energy sources such as natural gas.

In Vietnam and Indonesia, on the other hand, much emphasis has been placed on retiring relatively young coal-fired power plants. According to the International Energy Agency (IEA), the average age of coal plants in Southeast Asia is less than 15 years old, typically having a lifetime of 30 to 40 years. Under the 7th ASEAN Energy Outlook, the region would still require coal for energy generation until 2050.[7] Both Indonesia and Vietnam emphasise the necessity of capping emissions from coal used for energy generation and reducing the peak capacity of coal-fired power plants in their respective JETP plans. [8][9]

Lastly, balancing the JETP policy design and regulatory approach is critical. After all, removing coal from energy generation requires firm political commitments from policymakers. Indonesia pledged to stop building new coal power plants after 2023, with the exclusion of coal-fired power plants in the pipeline and captive plants.[10] Meanwhile, Vietnam vowed to accelerate the Direct Power Purchase Agreement (DPPA) regulation between generators and large electricity users without going through Vietnam Electricity (EVN), incentivising the private sector to boost renewable energy take-up in the country.[11]

CHALLENGES OF JETP IMPLEMENTATION

Despite the promising funding scale of JETPs, the mechanism to address energy transition in each recipient country received much criticism. Some of the criticisms of JETP roll-outs in the two Southeast Asian countries include the following:

The financing gaps for energy transition in Indonesia and Vietnam are still big even with JETP financing.

Significant financing gaps remain in JETP countries even with JETP financing. Indonesia, for instance, requires a staggering US$66.9 billion to fund over 400 priority projects aimed at achieving its power sector transition pathway goals by 2030. Despite receiving US$20 billion in JETP funding, Indonesia still faces a substantial 70% financing gap.[12] Similarly, Vietnam needs US$135 billion to overhaul its electricity sector, including stopping the issuance of permits for new coal plants and building new renewable power plants and upgrading its electricity grids.[13] Despite the infusion of US$15.5 billion in JETP funds, Vietnam confronts a towering 89% financing gap. Both countries still need to mobilise other sources such as public funding, private investments, or commercial loans to continue with their JETP plans.

Furthermore, there is criticism that the JETP financing package lacks attractiveness. According to Indonesia’s Comprehensive Investment and Policy Plan 2023 drawn up for its JETP, 60% of the first US$11 billion funding tranche will be in the form of a concessional loan, with grants and technical assistance making up only 3% of the total funding package.[14] Similarly, according to Vietnam’s Resource Mobilization Plan, 52% of the first US$8.5 billion tranche mobilised by IPG countries will be in the form of non-concessional loans.[15] In comparison, grants and technical assistance will comprise only 4% of the first tranche.

Source: Just Energy Transition Partnership Indonesia Comprehensive Investment and Policy Plan 2023

Source: Resource Mobilization Plan: Implementing Vietnam’s Just Energy Transition Partnership

Aligning donor and recipient countries’ expectations is challenging.

The JETP financing packages for Indonesia and Vietnam reflect a commercial approach, suggesting that IPG countries prioritise the marketability of energy transition. A coalition of experts in Indonesia recognises that most IPG countries direct their funding toward renewable energy generation and transmission rather than the decommissioning of coal plants.[16] Justifying the marketability of the latter presents greater challenges. Therefore, international assistance could play a more significant role in this area, instead of solely focusing on renewable energy investments already gaining traction from the private sector.

Furthermore, there is a lack of acknowledgement of the importance of community-based renewable energy projects for the energy transition, as indicated by both JETP plans from Indonesia and Vietnam. The high marketability standard imposed by donor countries could undermine the potential of small-scale, community-based renewable energy projects that promote development in rural areas and uphold people’s rights to better economic access and a just social transition.[17]

Moreover, while the majority of funding will come in the form of concessional loans with attractive interest rates, most concessional loans, especially if disbursed through established multilateral development banks (MDBs), will still require sovereign guarantees from host governments to assure lenders that the government will take certain remedial actions, should projects face challenges.[18] In reality, during unprecedented crises, host governments are forced to accept more risks such as volatile exchange rates.

The complex political-economic landscape of the coal industry

Both Vietnam and Indonesia rely heavily on coal for electricity generation and economic development. Coal has played a significant role in their energy mix due to its affordability and availability. Transitioning away from coal would necessitate substantial investments in alternative energy sources and could potentially disrupt existing economic structures.

While the momentum for renewable energy investment is gaining traction and various tools and policies are available for deployment, phasing out coal requires more than just technical execution. This is primarily due to the complex political-economic landscapes prevalent in coal-dependent countries. For instance, Indonesia grapples with challenges posed by influential coal lobbyists; the coal and mining sectors contribute up to 6 per cent of Indonesia’s GDP in 2021. Under President Jokowi’s first-term leadership, the country experienced a major decline in export markets for coal, thus prompting the influential coal industry to lobby for the construction of coal-fired power plants to raise domestic demand.[19] According to a report by Greenpeace, the coal mining sector is generously subsidised by state funds and coal lobbyists are strongly linked to politicians and ministers.[20] The report also highlights that after decentralisation in 1999, Indonesia saw a significant increase in the number of mining permits issued, rising from 750 in 2001 to more than 10,000 in 2010, a 13-fold increase, nearly half of which were for coal mining. This increase is attributed to politicians at regional and local levels being granted greater power to manage their resources, sometimes involving corruption and bribery.

In Vietnam, there is a common perception that the country’s rising attractiveness for foreign direct investment (FDI) is closely tied to its reliance on this inexpensive and widely available energy source. The Communist Party of Vietnam utilises the strategy of maintaining energy affordability and security to legitimise its power.[21] The electricity market in Vietnam is highly regulated, with the state-owned enterprise, Vietnam Electricity (EVN) being the largest buyer of electricity and holding a monopoly on transmissions and distribution. Currently, there is no regulation regarding the decommissioning of coal power plants, discouraging EVN from pursuing the termination of power purchase agreements with private suppliers.[22] The implementation of JETP in Vietnam was also tarnished by the government’s crackdown on several prominent environmentalists who are vocal anti-coal campaigners for alleged tax evasion, betraying its own JETP commitments.[23] These factors underscore the intricate challenges associated with transitioning away from coal in such contexts.

Concerns over the social impacts of energy transition

JETPs emphasise leveraging energy transition to unlock opportunities for inclusive development, thus necessitating the mainstreaming of the ‘just’ aspect in implementation. JETPs aim to provide an additional layer of protection for workers in the coal-generated energy industry (see Picture 1).

Picture 1 Workers’ Protection Diagram

Source: Writer’s Analysis

At the basic level, recipient countries typically have legislation mandating fundamental rights such as safety, health, freedom of association, and non-discrimination. Countries can further enhance these basic rights using international frameworks provided by the Sustainable Development Goals (SDGs) and the International Labour Organization’s Declaration on Fundamental Principles and Rights at Work, for instance. In addition to these fundamental rights, countries must expand workers’ protections, such as minimum salary and retrenchment compensation. Multilateral institutions like the World Bank and the Multilateral Investment Guarantee Agency offer various programmes to enhance these expanded protections. JETPs can play a pivotal role in strengthening another layer of protection, facilitating workers’ access to upskilling, reskilling, and involvement in company restructuring processes. This multifaceted approach enhances the inclusivity and fairness of energy transition initiatives, ensuring that they benefit all stakeholders, particularly workers, in a just and equitable manner.

The endeavour to mainstream a just transition should be approached comprehensively, encompassing not only quantitative outcomes but also the qualitative aspects of the process, such as the involvement of labour unions,[24] women, and indigenous communities in shaping policy decisions. In the context of ASEAN countries, the principle of just energy transition should also incorporate distributional justice, which calls for equal and equitable distribution of benefits and burdens related to energy production and consumption; procedural justice, which emphasises the equal and meaningful participation of all stakeholders in energy decisions; and recognition justice, which involves acknowledging the distinct and diverse identities and histories of people in affected communities.[25]

JETPS IMPLICATIONS FOR SOUTHEAST ASIA

In summary, international partners exhibit confidence in Southeast Asia’s institutional capacities and market prospects for energy transition. Both Vietnam and Indonesia, as two large markets in the region, have already become recipients of JETPs. The likelihood of the Philippines soon joining the JETP mechanism is high, as evidenced by a recent study published by the Rockefeller Foundation and the Environmental Defense Fund advocating for such participation.[26]

Additionally, exploring how JETPs can facilitate trade complementarity within the ASEAN region is pertinent. With Indonesia and Vietnam committed to enhancing renewable energy infrastructure, there will likely be an increased demand for components such as solar cells, semiconductors and battery storage. Other Southeast Asian countries with capabilities in manufacturing these components, such as Malaysia and Thailand, stand to gain from this increased demand. The current ASEAN Trade in Goods Agreement (ATIGA) can facilitate more low-carbon technology trade, thus fostering an intra-regional ecosystem to foster low-carbon technology manufacturing and consumption at scale.[27] However, Indonesia’s plan to downstream critical minerals[28] and enhance its capabilities for producing components for renewable energy might affect the region’s trade complementarity potential.

Furthermore, successfully scaling up renewable energy production and improving electricity grids in Indonesia and Vietnam may bolster their confidence in exporting electricity beyond their borders. This can be a welcome development for markets with high renewable energy demand, such as Thailand and Singapore.

CONCLUSION

The emergence of JETPs represents a significant step forward in global efforts to address climate change beyond the annual United Nations Climate Change Conferences (COPs). These initiatives, established during COP26, signal a commitment by the International Partners Group (IPG) to provide multilateral climate financing targeting energy transition, with a particular focus on assisting developing countries in transitioning away from coal. However, while the JETP financing mechanism demonstrates considerable promise in addressing energy transition challenges, several critical concerns remain, such as significant financing gaps, differing expectations and implementation standards between donor and recipient countries, the complex political-economic landscape of the coal industry in recipient countries, and concerns over the social impacts of energy transition.

Despite these challenges, JETPs offer momentum for Indonesia, Vietnam, and the region to accelerate their energy transition and unlock inclusive development. JETPs can serve as catalysts for energy transformation, allowing both countries to experiment with different financial strategies and strengthen governance structures for effective energy transition. The governance structure facilitated by JETPs to transition away from coal can serve as a springboard to crowdsource financial assistance from other international financing sources in the future.

ENDNOTES

For endnotes, please refer to the original pdf document.

| ISEAS Perspective is published electronically by: ISEAS – Yusof Ishak Institute 30 Heng Mui Keng Terrace Singapore 119614 Main Tel: (65) 6778 0955 Main Fax: (65) 6778 1735 Get Involved with ISEAS. Please click here: /support/get-involved-with-iseas/ | ISEAS – Yusof Ishak Institute accepts no responsibility for facts presented and views expressed. Responsibility rests exclusively with the individual author or authors. No part of this publication may be reproduced in any form without permission. © Copyright is held by the author or authors of each article. | Editorial Chairman: Choi Shing Kwok Editorial Advisor: Tan Chin Tiong Editorial Committee: Terence Chong, Cassey Lee, Norshahril Saat, and Hoang Thi Ha Managing Editor: Ooi Kee Beng Editors: William Choong, Lee Poh Onn, Lee Sue-Ann, and Ng Kah Meng Comments are welcome and may be sent to the author(s). |

2024/39 “Policies to Increase the Inclusiveness, Resilience and Sustainability of Economic Growth in Cambodia” by Jayant Menon

EXECUTIVE SUMMARY

- To realise its aspirations to become an upper middle-income country by 2030 and a high-income country by 2050, Cambodia has to pursue inclusive growth that is also sustainable and resilient. This is the type of growth that generates decent and sustainable jobs in the manufacturing and services sectors, and fair and sustainable returns for the self-employed, in the formal and informal sectors.

- A key constraint is the lack of diversification of the economy. This has not affected the rapid pace of economic growth but only the inclusiveness and sustainability of that growth.

- The early phase of diversification involving rural-urban migration from the agricultural sector into the industrial and services sectors may be reaching its limit; future increases in productivity will have to come from intra-sectoral diversification. This involves the vertical shift into higher value-added products and activities within each sector.

- Intra-sectoral diversification requires that two key constraints be addressed. First is limited human capital, calling for improvements in the quality of education at all levels, starting with primary and secondary before technical and tertiary education. Second is the high cost of doing business, which stems from limited physical and logistics infrastructure, high energy cost, and the high cost of finance.

- Addressing these constraints should increase inclusiveness in economic growth.

- To ensure that these achievements are not short-lived, another set of constraints that affect resilience and sustainability need to be addressed: (i) climate change and other environmental pressures; (ii) financial, health and other shocks or crises; and (iii) technological change, especially the acceleration towards a digital economy.

- Improving the sustainability of growth and its drivers involve diversifying trade and investment flows.

* Jayant Menon is Senior Fellow at ISEAS – Yusof Ishak Institute. He thanks Cassey Lee, Lee Poh Onn and participants at an ERDI Economics Seminar at the Economic Research Department at the ADB and the CDRI 2023 Cambodia Outlook Conference for useful comments, without implicating them in any way.

ISEAS Perspective 2024/39, 30 May 2024

INTRODUCTION

In many ways, Cambodia is Asia’s true miracle economy. It was only three decades ago when the Paris Peace Agreements were signed, ending the civil war that ensued following the ouster of the genocidal Khmer Rouge regime in 1979. In just over a generation, Cambodia has built up its economy and institutions almost from scratch, and transformed itself into a modern, thriving economy. Although many challenges remain, these achievements should be recognised and bode well for the future.

Despite its tragic history, Cambodia has great aspirations. It aims to become an upper middle- income country by 2030 and a high-income country by 2050. To realise these aspirations, Cambodia has to pursue inclusive growth that is also sustainable and resilient. This type of growth should generate decent and sustainable jobs in the manufacturing and services sectors, and fair and sustainable returns for the self-employed, either in agriculture or in the micro, small and medium enterprises (MSMEs) across sectors, formal or informal. To do this, it has to address a number of constraints.

A key constraint, which is highlighted in the Royal Government of Cambodia’s Rectangular Strategy (Phase IV) and the new Pentagon Strategy Phase I, is the lack of diversification in the economy.[1] Although highlighted in the ADB’s (2014) Country Diagnostic Study (CDS), it continues to be a major constraint. The lack of diversification may not have affected the rapid pace of economic growth, but may have hindered the quality of that growth, particularly its inclusiveness and sustainability. Cambodia has been able to grow at above an annual rate of 7% since the turn of the century, except for the years afflicted by the Global Financial Crisis (GFC) and the COVID-19 pandemic (Figure 1). This high growth was mainly driven by trade preferences, tourism centred around Angkor Wat, and large capital inflows mainly from China into infrastructure and real estate. With Least Developed Country (LDC) graduation expected this decade, Cambodia will become a victim of its own success, and trade preferences and aid flows are likely to diminish. It will need to pursue new drivers of growth, which will require new and greater diversification.

The early phase of diversification or structural transformation, involving rural-urban migration from the agricultural sector into the industrial and services sector, has been ongoing but may be reaching its limit. This inter-sectoral transfer of factors of production is the easy phase of diversification, requiring minimal government intervention or policy reform, and takes place somewhat naturally with minimal disruption to factor markets (see Kaldor, 1967; Herrendorf et. al., 2013). The horizontal shift across sectors into higher value products and activities produces a one-off increase in the level of productivity, which raises incomes and living standards; however, this increase may not be sustainable.

Future increases in productivity will have to come from intra-sectoral diversification or specialisation within sectors. This involves the vertical shift into higher value-added products and activities within the industrial, services and agricultural sectors. This type of diversification is sometimes referred to as moving up the value-chain by engaging in higher value-added activities and in manufacturing, and is associated with greater participation in global value or supply chains. Unlike the early phase of industrialisation, this process of upgrading is unlikely to happen naturally and will require government intervention and/or policy reforms.

There are two major constraints that need to be addressed through policy reforms and government support to enable greater intra-sectoral diversification. The first is limited human capital and skills mismatches. Second is the high cost of doing business, which limits development of the private sector and domestic and foreign investment. Addressing these two sets of constraints should result in economic growth that is more inclusive. To ensure that these achievements are not short-lived, another set of constraints need to be addressed. This involves measures designed to increase resilience and sustainability, which would otherwise threaten current and future growth.

To address these constraints, three accompanying sets of policy reforms and government interventions are recommended.

KEY CONSTRAINTS TO DIVERSIFICATION AND INCLUSIVE GROWTH

Human Capital

Starting with the human capital constraint, there is an urgent need to improve the quality of education at all levels, and not just Technical and Vocational Education and Training (TVET) or tertiary education. TVET and tertiary education can only succeed if students have had a strong educational foundation in primary and secondary schooling. Results from the 2022 Programme for International Student Assessment (PISA) show Cambodia lagging behind its ASEAN peers in math, science, and reading despite improvement since 2017 (Figure 2). Similarly, Cambodia lags in the share of its labour force with advanced education (Figure 3).

Quality improvements also need to be accompanied by measures to improve access and retention rates, which are currently low. For instance, Warr and Menon (2016) found that more than 30 percent of new employees in the Japanese multinational firm Denso had never attended school, could not read or write, and had limited numeracy skills. Although firms like Denso were willing to provide their own tailored and on-the-job training, these workers were effectively untrainable and could only be employed to undertake the most routine of manual tasks.[2]

Cambodia needs to invest in skills development and training in close collaboration with the private sector to avoid skills mismatches. TVET and tertiary education institutions need to align their curricula more closely with the needs of the private sector. There is also a pressing need to address the various barriers and push-and-pull factors that limit access to formal employment, and strengthen social protection systems.

Business Costs

Second is the high cost of doing business, which stems from limited physical and logistics infrastructure, high energy cost, and the high cost of finance. For a developing economy like Cambodia that is rapidly transforming, transport and related infrastructure needs are a moving target. Despite notable achievements in building infrastructure, a deficit remains which continues to add significantly to business costs. There is a need to prioritise investments both within the transport sector, as well as economy-wide. Within transport, chokepoints such as port capacity, high-cost centres such as logistics infrastructure, and inter-modal connectivity should be prioritised.

Since infrastructure development relies on foreign involvement, increasingly from China through the BRI, there is a need for better vetting of project proposals through comprehensive cost-benefit analyses conducted by an independent body. It is time for the country to consider setting-up an independent Foreign Investment Review Board, operating as a non-statutory body with inter-ministerial and multi-stakeholder representation, to assess individual proposals in a purely advisory capacity. The inter-ministerial representation would ensure that sector priorities are considered in the approval process (see Menon, 2024).

The cost of electricity in Cambodia is one of the highest in the region, with a kilowatt hour costing USD 0.14 relative to 0.11 in Thailand and 0.08 in Vietnam. The high cost is limiting vertical upgrading within electronics and automotive supply chains, from labour-intensive

assembly activities to higher value-added, energy intensive production of parts and components. Greater investment in renewable energy and energy efficiency is required to reduce costs as well as the reliance on diesel and heavy fuel oil in electricity generation. Investment in grid extension and addressing the fragmented nature of transmission and distribution will reduce the cost of electricity. There is significant potential to scale up investment in solar energy, which could significantly reduce business costs for MSMEs that are off grid.

The high cost of finance, especially to small-scale farmers and MSMEs, perpetuates poverty (Karamba et. al., 2022). Limited access to formal avenues of finance, with more than 70 percent of the population estimated to be unbanked, is closely related to its high cost. The potential for digital innovation, including fintech and blockchain, presents significant opportunities for Cambodia’s financial sector to enhance financial inclusion. Increasing digital literacy and access to digital infrastructure, which is still low in the rural sector, is required to increase access of the poor to finance at a reasonable cost.

There are also a host of long-term development challenges that need to be addressed which will affect trust in the system, and therefore both the access to and the cost of finance. These include issues relating to governance and corruption, the quality of institutions including the legal system, and the development of the finance sector and capital markets.

LONG-TERM INCLUSIVE GROWTH: INCREASING RESILIENCE AND SUSTAINABILITY

To ensure that growth is more inclusive not just in the short term but extends into the long term, there is a need to reduce the risk of disruptions while increasing the versatility in managing and responding to all kinds of shocks. Increasing resilience include addressing the impacts of: (i) climate change and other environmental pressures; (ii) financial, health and other shocks or crises; and (iii) technological change, especially the acceleration towards a digital economy. Improving the sustainability of growth and its drivers involve diversifying trade and investment flows; diversifying export products and markets and import sources, as well as sources of FDI flows, will reduce risk and increase the sustainability of economic growth. Policies and interventions to address each of these are discussed in turn, below.

Climate change and other environmental pressures

Climate change threatens the livelihoods of millions as well as long-term aspirations such as reaching high-income status by 2050. ADB (2023) estimates that Cambodia’s GDP could be up to 10% lower than otherwise in 2050.

While economic growth and environmental protection are often considered trade-offs, there can nevertheless be complementarity between them. The intersection between the two is green growth, where ecologically sustainable economic growth that fosters low carbon but socially inclusive development is the outcome. Green investments do not only unlock growth potential but also create decent and sustainable jobs for the future. There is significant potential to scale up investment in renewable energy and energy efficiency using Cambodia’s solar energy resources.[3] Significant parts of Cambodia remain without access to electricity, and solar power carries the potential of transforming remote and often poor communities by providing them with affordable clean energy and the opportunity to improve living conditions

Transitioning away from the heavy reliance on fossil fuels, reducing the rate of deforestation and adopting more sustainable agricultural and fishing practices will be critical in protecting the environment and ensuring the future prospects of these industries.

As green and sustainability aspects of production become increasingly important in business and investment decisions of international firms, reducing Cambodia’s carbon footprint would present it with new growth opportunities that arise from increasing global demand for environmentally sustainable products and services.

Financial, health, and other shocks or crises

- Financial Risks

Cambodia will need to strengthen its financial sector resilience by enhancing regulatory and supervisory frameworks, improving asset quality and risk management practices, and addressing weaknesses in the banking system. There is a need to implement regulations to deal with bank and debt restructuring, and corporate insolvency. Rising private debt following the slump in the property market has also become a concern that could threaten the stability of the economy and its future growth. The IMF (2024) notes that its share of GDP at around 160 percent is high for a country at Cambodia’s level of development.

With the growth in shadow banking and the increase in non-bank financial institutions, greater regulatory oversight and supervision will be required. Cambodia’s authorities will also need to accelerate work on a deposit protection scheme, implement measures to prevent money laundering, and clarify the framework for bank resolution.

Cambodia’s authorities will need to carefully monitor the health of banks and microfinance institutions as the forbearance measures are phased out, especially the systemically important banks that have high exposure to the construction and real-estate sector. A staged increase in minimum capital requirements could also be used to promote consolidation in the banking and microfinance sectors.

- Health crisis

Although Cambodia did remarkably well in managing the COVID-19 pandemic, it highlighted a number of vulnerabilities in the healthcare system that need to be addresses before the next health emergency occurs. Government spending on healthcare needs to be significantly increased in preparation for the next pandemic or major public health outbreak.[4] This was a major limitation in managing the COVID-19 pandemic, requiring more stringent controls than in countries with more robust healthcare systems.

There is great variation in access to quality healthcare in the urban versus rural sector. There is a pressing need to increase both the access and the quality of healthcare in remote regions, that are currently poorly served. Unless there is greater investment to increase the quality and quantity of healthcare services, any future health crisis requiring mass hospitalisation could quickly overwhelm the healthcare system, inflicting a larger than necessary human and economic toll.

- Technological change, especially the acceleration towards a digital economy

The acceleration towards a digital economy will produce many benefits, but it will also create new challenges. Many low- and medium-skilled jobs may be lost initially, although Artificial Intelligence threatens even highly skilled ones. It will not be easy to redeploy low-skilled workers, and reskilling and retraining will be required. Despite the anti-globalisation backlash elsewhere, Cambodia must remain open to importing skills and technology to help it catch up in the short run. In the long run however, the challenges posed by digitalisation and rapid technological change will require a fundamental transformation in systems of education and learning. Indeed, the digital transition reinforces the need to address the underlying problems associated with human capital and skills development discussed earlier. Augmenting cognitive skills such as math’s and sciences will be critical for the transition to a more innovative, knowledge-based economy. New and innovative approaches to public-private collaboration are also needed, particularly in areas such as research and development.

- Diversifying export markets and import sources

Cambodia’s trade patterns – both the commodity and country composition of its exports and imports – are highly concentrated, raising its vulnerability to country- or commodity-specific shocks. As the major constraints to structural diversification such as limited human capital and high business costs are addressed, trade and investment flows will also diversify. For instance, if the price of electricity could be reduced, this could attract new types of FDI from different source countries, which would result in new types of output such as electronic parts and components. This alters both the commodity and country composition of exports and imports, helping to diversify trade and investment patterns. This is one of a number of indirect channels involving policy reform that can affect trade and investment patterns. The loss of trade preferences following LDC graduation will also help diversify export products and patterns naturally.

There are specific policy changes that can be pursued to deliberately diversify trade and investment flows, and directly improve its sustainability.

Preferences are also present in the many FTAs that Cambodia is engaged in that skew the commodity and country composition of its imports. The margin of preference (MOP) — the difference between preferential and Most-Favoured-Nation (MFN) rates — is still high for many tariff lines and across different FTAs in Cambodia. When MOPs are high, trade patterns can be distorted through trade diversion. It increases concentration of trade flows by diverting them from non-FTA partners to FTA partners. Trade diversion is also welfare-reducing because imports are no longer sourced from the lowest cost producer. Pursuing open regionalism through multi-lateralisation of FTA preferences – i.e., offering preferences to all countries on an MFN basis – is in Cambodia’s national interest. It would promote domestic competitiveness and welfare, while reducing the concentration in trade patterns (see Menon, 2022).

Diversifying sources of FDI

Cambodia needs to attract FDI or incur external debt if it is to grow at a rate faster than that determined by its low domestic savings rate. There is a sustainability element associated with both FDI and debt. The need for long-term debt sustainability is widely recognised and better understood than the need to ensure that FDI inflows do not exceed absorptive capacity. The latter is associated with ensuring that external competitiveness of the tradable goods sector is not impaired by a sharp appreciation of the real exchange rate due to massive inflows of FDI, resulting in Dutch Disease-type effects.[5] The relevant point here is that an economy like Cambodia should be selective in its choice of projects, whether financed by foreign investment or borrowings, if it is to grow in a sustainable and inclusive manner. In addition, increasing the share of new investors that can help plug Cambodia into new markets and manufacturing global supply chains will support domestic structural changes by diversifying sources of growth.

CONCLUSION

Cambodia aims to become an upper middle-income country by 2030 and a high-income country by 2050. To realise these aspirations, Cambodia has to pursue inclusive growth that is also sustainable and resilient. A key constraint is the lack of diversification of the economy, which has so far not affected the rapid pace of economic growth but only the inclusiveness and sustainability of that growth. Diversification so far has involved rural-urban migration from the agricultural sector into the industrial and services sectors, but this process may be reaching its limit. The horizontal shift across sectors into higher value products and activities produces a one-off increase in the level of productivity; future increases in productivity will have to come from intra-sectoral diversification. This involves the vertical shift into higher value- added products and activities within each sector.

Two key constraints limit the extent of intra-sectoral diversification. First is inadequate human capital, requiring improvements in the quality of education at all levels, starting with primary and secondary schooling. Second is the high cost of doing business, which stems from limited physical and logistics infrastructure, high energy cost, and the high cost of finance. Addressing these constraints should increase the inclusiveness of economic growth.

To ensure that these achievements last beyond the short term, another set of constraints that affect resilience and sustainability need to be addressed. Increasing resilience includes addressing the impacts of climate and technological change, and reducing the risk of financial, health and other crises but, should they occur, also mitigating their worst impacts. Improving the sustainability of growth and its drivers involve diversifying trade and investment flows. This will reduce Cambodia’s exposure to country-specific shocks and indirectly help with diversification of the economy.

REFERENCES

ADB. 2014. Country Diagnostic Study: Cambodia, Diversifying beyond Garments and Tourism. Manila. https://www.adb.org/sites/default/files/publication/149852/cambodia-diversifying-country- diagnostic-study.pdf.

———. 2023b. Asian Development Outlook, April 2023. Manila. https://www.adb.org/publications/asian-development-outlook-april-2023.

Herrendorf, B., R. Rogerson, and Á. Valentinyi. 2013. Growth and Structural Transformation. NBER Working Paper 18996. Washington, DC: National Bureau of Economic Research. http://www.nber.org/papers/w18996

IMF. 2024. Cambodia: 2023 Article IV Consultation-Press Release; and Staff Report. 31 January. Washington, DC. https://www.imf.org/en/Publications/CR/Issues/2024/01/29/Cambodia-2023- Article-IV-Consultation-Press-Release-and-Staff-Report-544276

Kaldor, N. 1967. Strategic Factors in Economic Development, Ithaca, NY: Cornell University.

Karamba, W., K. Tong, and I. Salcher. 2022. Cambodia Poverty Assessment: Toward a More Inclusive and Resilient Cambodia. Washington, DC: World Bank. http://hdl.handle.net/10986/38344.

Menon, J. 2022. The CLMV Countries and RCEP: Will They Grasp the Opportunities? Fulcrum. 18 February. https://fulcrum.sg/the-clmv-countries-and-rcep-will-they-grasp-the-opportunities/

———. 2024. The Belt and Road Initiative in Cambodia: Costs and Benefits. Journal of Southeast Asian Economies. 41 (2), pp. 1-12. ISEAS_EWP_2023- 1_Menon.pdf.

Menon, J. and K. Naqvi. 2024. Structural Transformation and Growth Opportunities in Cambodia: A Product Space Analysis, Paper prepared for the Striving for Inclusive Economic Growth in Asia and the Pacific Conference, ADB and ADB Institute, Manila, forthcoming.

UNDP. 2019. Cambodia: Derisking Renewable Energy Investment. New York: United Nations Development Programme. https://www.undp.org/sites/g/files/zskgke326/files/2022- 09/DREI%20Cambodia%20Full%20Report%20%28English%29%20%28Jun%202019%29%20%28 FINAL%29.pdf.

Warr, P. and J. Menon. 2016. Cambodia’s Special Economic Zones. Journal of Southeast Asian Economies. 33 (3), pp. 273–90. https://www.adb.org/sites/default/files/publication/175236/ewp- 459.pdf.

ENDNOTES

For endnotes, please refer to the original pdf document.

| ISEAS Perspective is published electronically by: ISEAS – Yusof Ishak Institute 30 Heng Mui Keng Terrace Singapore 119614 Main Tel: (65) 6778 0955 Main Fax: (65) 6778 1735 Get Involved with ISEAS. Please click here: /support/get-involved-with-iseas/ | ISEAS – Yusof Ishak Institute accepts no responsibility for facts presented and views expressed. Responsibility rests exclusively with the individual author or authors. No part of this publication may be reproduced in any form without permission. © Copyright is held by the author or authors of each article. | Editorial Chairman: Choi Shing Kwok Editorial Advisor: Tan Chin Tiong Editorial Committee: Terence Chong, Cassey Lee, Norshahril Saat, and Hoang Thi Ha Managing Editor: Ooi Kee Beng Editors: William Choong, Lee Poh Onn, Lee Sue-Ann, and Ng Kah Meng Comments are welcome and may be sent to the author(s). |

2024/38 “Ethnic Diversity in Kalimantan and the Implications of Indonesia’s Capital Relocation” by Evi Nurvidya Arifin

EXECUTIVE SUMMARY

- This article provides foundational statistics on the ethnic mosaic in Kalimantan and delves into the intricate dynamics of the ethnic diversity of Borneo island. This ethno-demographic exploration is conducted through a political economy lens.

- Among the diverse regions in the country, Kalimantan stands out as one of the most culturally complex societies with at least ten ethnic groups identified, with Banjarese emerging as the largest group, followed by the Dayak, Javanese, Malay, Batak, Madurese, Chinese, Kutai, Sundanese, and Buginese.

- While three provinces in Kalimantan are dominated by local ethnic groups, the Javanese make up the largest group in East Kalimantan, where the new capital, Nusantara, will be located.

- This article also offers an understanding of socio-demographic-political dimensions intertwined with the ethnic fabric of Kalimantan, thereby contributing to the broader discourse on Indonesia’s diverse landscape and its implications for governance and development initiatives.

ISEAS Perspective 2024/38, 29 May 2024

* Evi Nurvidya Arifin is Senior Assistant Professor at the Centre for Advanced Research (CARe), Universiti Brunei Darussalam. Her research areas encompass ethnicity, religion, electoral behaviour, ageing population, internal and international migration, poverty, retirement, disability, fertility and reproductive health. This paper was originally presented at the Religious Diversity in Borneo Workshop in 2023.

INTRODUCTION

The significance of understanding ethnic diversity in Kalimantan has been magnified in recent times, particularly in light of the grand plan to relocate Indonesia’s capital city. With Prabowo Subianto and Gibran Rakabuming Raka’s victory in the 2024 presidential elections and the pair’s commitment to continue this monumental project initiated by President Joko Widodo (Jokowi), the intricacies of the ethnic composition in Kalimantan take on heightened importance.

The decision to shift the capital from Jakarta to East Kalimantan underscores a practical necessity to alleviate the congestion and environmental challenges plaguing Jakarta, and represents a strategic move towards decentralization and regional development. However, this ambitious endeavour is not without its complexities, especially concerning the diverse ethnic landscape of Kalimantan.

As Prabowo and Gibran assume office and move forward with the capital city relocation plan, understanding the nuances of ethnic diversity in Kalimantan becomes imperative. This understanding is crucial for ensuring the successful implementation of policies and initiatives that respect the region’s cultural, social, and economic realities.

Kalimantan is the expansive Indonesian territory on the island of Borneo which is considered the world’s third largest.[1] It is a region abundant in cultural heritage and diversity. This diversity has long shaped its social fabric, economic activities, and political landscape. The planned relocation will begin as early as this year. Therefore, Borneo will become the centre of integrated socio-economic activities and geopolitics in the future, where three Southeast Asian countries (Indonesia, Malaysia, and Brunei) are located, along with two capital cities, namely Nusantara and Bandar Seri Begawan.

Kalimantan is known as the “Island with a Thousand Rivers”. Its rivers have historically served as important transportation arteries. Many continue as essential routes for the transportation of people, goods and services. Kalimantan’s cultural and religious landscape has been significantly transformed due to historical events such as the transmigration policy in the colonial era and post-independence,[2] as well as subsequent economic migration, religious conversions, and socio-economic influences.

Empirical studies in many different countries have provided an understanding of how ethnic diversity relates to different aspects of development, such as democratisation, economic growth, income inequality, corruption, and wellbeing. In their seminal paper, Easterly and Levine showed that a higher degree of ethnic diversity can lower the growth rate of GDP per capita.[3] Many other studies have examined the negative relationship between ethnic diversity and economic growth.[4] It is important to note that an ethnically diverse region is not automatically more prone to internal conflict.[5] The likelihood of that can increase if the region is polarised. More recent research on the varying relationships between ethnic diversity and economic growth suggests that ethnic diversity may be beneficial to economic growth, although this may depend on the level of the administrative unit under analysis.[6] Ethnic diversity plays a crucial role in mediating between internal migration and economic growth in Indonesia.[7] If ethnic diversity is a spur to innovation, productivity, and trade among districts, then migration needs to be “managed” for regions to obtain economic benefits while minimising adverse social and political effects.[8]

This article provides foundational statistics on the ethnic mosaic in Kalimantan and explores the intricate dynamics of ethnic and religious diversity through the lens of political economy and demography, contextualised within the framework of the capital city relocation project.

HISTORICAL CONTEXT

Despite Indonesia’s acknowledgment of diversity, a significant lack of information regarding ethnicity existed from 1930 to 2000. Since attaining Independence in 1945, the national motto, “Bhinneka Tunggal Ika” or “Unity in Diversity,” has served as the guiding principle for all Indonesians. The period following the fall of Suharto’s New Order regime (1967-1998) and the subsequent transition to a more democratic setting witnessed a pivotal moment, with the first population census in 2000 marking a breakthrough in quantifying ethnic groups across all Indonesian islands.[9]

Kalimantan is characterised by a rich mosaic of indigenous cultures and external influences. The region has long been inhabited by diverse Dayak communities, each nurturing its unique traditions, languages, and socio-political structures. These historically embraced animism and held deep reverence for the natural environment, shaping profound connections between land and spirituality.[10]

Islam predated colonial powers, and Muslim communities particularly resided along the riverbanks. The 16th century witnessed widespread conversion to Islam, notably in South Kalimantan, where Sultan Suriansyah became the first to embrace the faith.[11] The support of local sultanates across South, West, Central, and North Kalimantan significantly influenced this conversion trend. However, the advent of external powers, such as the Dutch and British colonial administrations, profoundly impacted the ethnic and religious fabric of Kalimantan.[12] Colonial expansion reshaped governance structures, economic systems, and cultural practices, integrating Kalimantan into broader trade and commerce networks. Moreover, the colonial era saw the propagation of Islam and Christianity, introducing new religious dynamics to Kalimantan.[13] While Islam gained prominence among coastal communities through trade and missionary endeavours, Christianity found adherents among select Dayak groups, contributing further to the region’s diverse religious landscape.

The evolution of Kalimantan’s political economy and legal frameworks has been deeply intertwined with its ethnic and religious diversity. Colonial administrations implemented policies that often favoured certain ethnic and religious groups over others, leading to social stratification and tensions within the region.[14]

Post-independence, efforts were made to foster national unity while respecting the diversity of Kalimantan’s communities. The Indonesian government implemented policies aimed at promoting cultural pluralism and religious tolerance, enshrining these principles in the nation’s constitution.

The historical legacies of colonization and cultural exchange continue to influence contemporary issues in Kalimantan. Ethnic tensions persist, exacerbated by socio-economic disparities, political marginalization, and competing claims to land and resources. Furthermore, the rapid pace of development and urbanization in Kalimantan has brought new challenges, such as environmental degradation, loss of indigenous land rights, and cultural erosion.

ETHNIC DIVERSITY IN KALIMANTAN

Kalimantan is a significant geographical and demographic entity, comprising 915 smaller islands, with a sprawling land area spanning 544,150.07 square kilometers. As of 2020, Kalimantan accommodated approximately 16.63 million inhabitants, constituting 6.0% of Indonesia’s total population and a substantial increase from its 1971 figure of 5.15 million, representing 4.3% of the nation’s population. Kalimantan harbours 72.2% of Borneo’s total population, underscoring its demographic weight within the island.

This surge in population can be attributed to a confluence of factors including natural population increase and significant migration flows. Migration, facilitated both by the government’s transmigration policy and voluntary movements, has been an influential driver of population growth and change in Kalimantan. The influx of Javanese migrants into this region accelerated changes in economy and society.[15] The region’s allure, characterised by promising economic opportunities, available land, and abundant natural resources, has attracted individuals from various parts of Indonesia seeking to capitalise on these prospects. The influx of migrants from diverse regions further enriched the cultural fabric of Kalimantan. Moreover, these population movements have played a crucial role in economic development.

Despite the overall demographic growth, disparities among Kalimantan’s provinces are evident. West Kalimantan emerges as the most populous province, boasting a population of 5.4 million in 2020. In contrast, North Kalimantan, the newest province separated from East Kalimantan, accommodated the smallest population, with only 0.7 million inhabitants in 2020. However, projections suggest that its population may experience accelerated growth in the future.

Kalimantan is home to at least 16 distinct ethnic groups (Banjar, Dayak, Javanese, Malay, Batak, Madurese, Chinese, Kutai, Buginese, Sundanese, Toraja, Pasir, Butonese, Balinese, Mandar, and Flores). However, only four—Banjarese, Dayak, Kutai, and Pasir—originated from Kalimantan, with others being migrant ethnic groups from different parts of Indonesia.[16] The Banjarese, the largest group in Kalimantan, constituted 26.2% or 3.6 million people in 2010. Banjarese identified themselves as Banjarese or as being affiliated with sub-ethnic groups like ‘Banjar Kuala,’ ‘Batang Bunyu,’or ‘Pahuluan.’ The Dayak people, approximately 3 million, represent the most culturally diverse local ethnic group consisting of 375 sub-ethnic groups.18

Kutai also emerges as a separate local ethnic group with around 276,000 individuals, constituting 2% of Kalimantan’s population in 2010. Pasir, an indigenous local ethnic group in East Kalimantan, is distinct from the Dayak Pasir. Pasir made up about 0.5 percent of the population, exclusively residing in East Kalimantan. Other significant migrant ethnic groups in Kalimantan include the Javanese (18.2 %), Malay (originating from Sumatra, 11.4 %), and Batak (from North Sumatra, 5.7 %).

Ethnic diversity among provinces in Kalimantan varies significantly (Figure 1). West Kalimantan is geographically strategic, bordered by Sarawak, Malaysia, and the South China Sea. It is home to the two largest ethnic groups: Dayak (34.9%) and Malay (33.8%), both culturally distinct.

Figure 1. Ethnic composition among provinces in Kalimantan

In Central Kalimantan, Dayak is the largest group, and it coexists with Banjarese from South Kalimantan and Javanese from Java Island. However, South Kalimantan is predominantly Banjarese. By contrast, East Kalimantan is a migrant province with the three largest ethnic groups being Javanese, Buginese and Banjarese. North Kalimantan which was separated from East Kalimantan and established in 2012, has a different ethnic composition, with Buginese as the largest group, followed by Dayak and Javanese.

Each ethnic group in Kalimantan brings unique skills, knowledge, and contributions to the region’s socio-economic fabric. The Dayak communities, for example, have traditionally relied on agriculture, fishing, and hunting for their livelihoods, while also practising crafts such as weaving and wood carving. The Malay and Javanese communities have been actively involved in trade, commerce, and government administration. Trade networks, cultural exchanges, and intermarriages have historically fostered connections and mutual understanding among different ethnic groups. Festivals, ceremonies, and religious events provide opportunities for people from diverse ethnic backgrounds to come together, celebrate their shared heritage, and forge bonds of solidarity.

Like in other such places, Kalimantan has experienced ethnic conflicts, albeit sporadically, throughout its history. After the fall of the New Order regime in 1998, several ethnic violent clashes took place in the provinces of West, Central and East Kalimantan. Some studies have endeavoured to comprehend the underlying causes of the outbreak of violent conflict. For example, conflicts have been linked to intense competition for economic opportunities, particularly concerning agricultural resources among Malays, Dayaks, and Madurese communities in West Kalimantan,[17] and illegal lodging in Central Kalimantan.[18] This competition engendered feelings of frustration and aggression.

On the other hand, during the decentralization era, there has also been increased recognition of the need for greater political participation and for empowerment of ethnic minorities in Kalimantan. For example, Singkawang is unique in Indonesia as the only district where the Chinese ethnic group is the largest, although not the predominant one. With a Muslim majority, this district was run for the first time by a Chinese lady, Singkawang-born Tjhai Chui Mie, from December 2017 to December 2022.[19] Tjhai Chui Mie’s tenure as female leader in a traditionally male-dominated field demonstrates that women can hold significant positions of power and influence in the political sphere and in local governance. This reflects a notable progress in gender empowerment and leadership diversity.

However, power dynamics within Kalimantan’s political landscape remain complex, with entrenched interests and historical inequalities shaping the distribution of resources and opportunities. Achieving greater representation and inclusivity will require ongoing dialogue, collaboration, and policy reforms that prioritise the needs and aspirations of all ethnic groups in the region.

POLITICAL ECONOMY AND ETHNIC DYNAMICS

Kalimantan is economically vital, enriched with abundant natural resources like timber, minerals, and oil and gas reserves. Industries such as mining and palm oil production have flourished, with East Kalimantan ranking second in wealth after Jakarta since the 1970s, contributing 9.2% to the total gross regional product by 2010.

The upcoming establishment of Nusantara, Indonesia’s new capital city, in East Kalimantan is set to spur further economic growth. This initiative is expected to attract significant investments, create jobs, and draw professionals and businesses to the province. However, it may also lead to demographic changes that affect the ethnic composition of local communities.

Upon closer examination of ethnic groups at the district level in East Kalimantan, it becomes apparent that the region’s economy is significantly influenced by migrant populations. This influence is reflected in the ethnic composition in various districts throughout the province. Several districts prominently feature the Javanese ethnic group as the largest, including Paser, Kutai Kartanegara, East Kutai, North Penajam Paser, Balikpapan, Samarinda, and Bontang. This suggests that the economy of East Kalimantan is largely driven by migrants, particularly those of Javanese descent.

Moreover, with the planned establishment of Nusantara in Javanese-majority districts of Kutai Kertanegara and North Penajam Paser, this influence is expected to strengthen in the future. Conversely, districts such as West Kutai, Malinau, Bulungan, and Tana Tidung have the Dayak population as the largest ethnic group. This highlights the ethnic diversity within East Kalimantan and underscores the importance of recognizing and respecting the cultural heritage and contributions of indigenous communities in the region.

While ethnic diversity offers economic opportunities such as a vibrant tourism industry and diverse skillsets, it can also create tensions, especially if newcomers seek dominance in economics and politics. Economic disparities may arise from unequal resource access, affecting marginalised communities. Efforts to address these issues require equitable policies and community empowerment initiatives.

By aligning governmental policies with principles of social justice and equality, Kalimantan can harness the economic potential of its diversity while promoting inclusive growth.

CONCLUSION

The significance of understanding ethnic diversity in Kalimantan has been underscored by recent developments, particularly the plan to relocate Indonesia’s capital city to East Kalimantan. This ambitious endeavour highlights the need to navigate the complexities of ethnic composition and dynamics in the region. The decision to shift the capital not only addresses practical concerns such as alleviating congestion and environmental challenges in Jakarta but also signifies a strategic move towards decentralization and regional development.

With its rich cultural heritage and diversity, Kalimantan stands as a unique region shaped by historical events, colonial influences, and socio-economic transformations. The planned relocation project, scheduled to begin in 2024, is expected to position Borneo as a centre of integrated socio-economic activities and geopolitics in the future, with two capital cities located within its boundaries.

Ethnic diversity in Kalimantan, characterised by at least 16 distinct ethnic groups, underscores the region’s status as a melting pot of cultures and traditions. While some groups, such as the Banjarese and Dayak, have indigenous roots in Kalimantan, others have migrated from different parts of Indonesia. Despite disparities among provinces, ethnic diversity permeates various aspects of life in Kalimantan, from socio-economic activities to political dynamics.

The economic vitality of Kalimantan, driven by industries like mining and palm oil production, is poised for further growth with the establishment of Nusantara. However, this development may bring changes that impact the ethnic composition of local communities.

Efforts to promote greater representation and inclusivity require ongoing dialogue, collaboration, and policy reforms that prioritise the needs and aspirations of all ethnic groups in Kalimantan. By aligning governmental policies with principles of social justice and equality, Kalimantan can harness the economic potential of its diversity while fostering inclusive growth and sustainable development in the region.

ENDNOTES

For endnotes, please refer to the original pdf document.

| ISEAS Perspective is published electronically by: ISEAS – Yusof Ishak Institute 30 Heng Mui Keng Terrace Singapore 119614 Main Tel: (65) 6778 0955 Main Fax: (65) 6778 1735 Get Involved with ISEAS. Please click here: /support/get-involved-with-iseas/ | ISEAS – Yusof Ishak Institute accepts no responsibility for facts presented and views expressed. Responsibility rests exclusively with the individual author or authors. No part of this publication may be reproduced in any form without permission. © Copyright is held by the author or authors of each article. | Editorial Chairman: Choi Shing Kwok Editorial Advisor: Tan Chin Tiong Editorial Committee: Terence Chong, Cassey Lee, Norshahril Saat, and Hoang Thi Ha Managing Editor: Ooi Kee Beng Editors: William Choong, Lee Poh Onn, Lee Sue-Ann, and Ng Kah Meng Comments are welcome and may be sent to the author(s). |

2024/37 “Bleak Future for Islamic Parties in Indonesia after the 2024 Election” by Pradana Boy Zulian and Neni Nur Hayati

EXECUTIVE SUMMARY

- The recently concluded 2024 Indonesian legislative election raises questions about the future of Islamic political parties. Their last strong showing was in the 1955 election, after which they have been experiencing a slow decline. They are now on the periphery of the country’s political arena.

- Only the National Awakening Party (PKB) and the Prosperous Justice Party (PKS) increased their vote share in the 2024 election. Others, such as the United Development Party (PPP) and People’s Party (Partai Ummat), a new Islamic party founded by reform icon Amien Rais, failed to secure any parliamentary seats.

- Islamic political parties are thinly spread. Moreover, there is no correlation between their affiliation with Islamic organisations and choice of political party. Nahdlatul Ulama (NU) members do not automatically vote for PKB; the same is true of Muhammadiyah’s relationship with the National Mandate Party and Partai Ummat.

- Among Indonesian Islamic parties, PKS’ future is the brightest and this is due to the loyalty of its support base. PKS’ Islamist ideology—inspired by the Muslim Brotherhood in Egypt—is developed for a further goal of founding an Islamic state in Indonesia and pushing for the Islamisation of Indonesian society. These ideas and beliefs foster strong political aspirations and have successfully bound members to the party.

ISEAS Perspective 2024/37, 21 May 2024

* Pradana Boy Zulian is Visiting Fellow with the Regional Social and Cultural Studies Program at ISEAS – Yusof Ishak Institute. Neni Nur Hayati is the Director of the Democracy and Electoral Empowerment Partnership (DEEP), in Indonesia.

INTRODUCTION

In Indonesia’s political history, Islamic parties, collectively, have never been a dominant force. Their best performance was in the 1955 election, the Republic’s first. Back then, the total vote percentage gathered by them was 43.5 percent. Of the four parties with the highest voters, two were Islamic parties, Masyumi (7,903,886 votes) and Nahdlatul Ulama (NU) (6,955,141 votes), with the other two being Partai Nasional Indonesia (PNI) (8,434,653 votes), and Partai Komunis Indonesia (PKI) (6,179,914 votes).[1]

However, after 1955, Islamic parties underwent a steady decline. The trend continued during the Suharto New Order period (1966–1998). Even in the post-New Order period, after political restrictions were lifted and political space opened for all groups, Islamic parties never managed to repeat their 1955 showing.

Throughout the Reformasi era, the vote share of Islamic parties swung between 16 percent and 30 percent.[2] The Islamic parties’ vote share from year to year are as follows: 1971 election (26.0 percent), 1999 election (36.8 percent), 2004 election (38.1 percent), and 2009 election (29.0 percent). The 2024 election recorded a similar pattern. If the National Mandate Party (PAN) is considered “Islamic” and included, then all Islamic parties gained about 30 percent. But if PAN is excluded, then Islamic parties only secured about 23 percent of the popular vote. In the past, PAN was undoubtedly categorised as an Islamic party. However, in recent years, some have questioned whether it can be considered as such, since its primary motivation is national development despite it originating from Muhammadiyah, the second largest Islamic organisation in Indonesia. A split within PAN’s ranks further fuelled questions of its Islamic identity. On 29 April 2021, PAN’s key founder, Amien Rais, founded the splinter Partai Ummat to move in a more conservative Islamic direction.

Considering this historical fact and current political dynamics in the country, discussing the future of Islamic parties becomes very important. This article argues that although Islamic parties showed partial improvements in the latest election, they will nevertheless remain stagnant and will not play any significant role in the future. Their prospects will not change much as long as they do not move beyond sectarian politics. Unless they can be sensitive towards rapid changes in Indonesian society, their ability to compete for political significance will remain weak.

Be that as it may, one party that deserves scrutiny is the PKS. Although it is unlikely to make any major inroads in the country’s politics or increase Islamic parties’ overall performance in the national polls, it enjoys much stronger loyalty from its members and supporters than its Islamic counterparts are able to do.

This article will analyse several factors contributing to the Islamic parties’ abysmal performance and examine their future trajectory. It considers the following trends: Islamic parties are not the main preference for Muslims in Indonesia; although all Islamic parties strive for the upholding of Islamic teachings, their goals are fragmented; and there is a disjuncture between voters’ religious ideology and political loyalty.

ISLAMIC PARTIES NOT MUSLIMS’ GIVEN CHOICE

Muslims do not automatically vote for an Islamic party. Only in the 1955 election—the first ever held in the country—did Islamic parties demonstrate a strong showing; two of them were among the top four parties then. In 2024, the votes gained by Islamic parties are as follows: the National Awakening Party (PKB) gained 10.62 percent, followed by the Prosperous Justice Party (PKS) at 8.42 percent, the United Development Party (PPP) at 3.87 percent and Partai Ummat at 0.42 percent. The last two—PPP and Partai Ummat—were left with no seat in parliament. Based on the Indonesian parliamentary threshold, a political party must secure a minimum of four percent of the popular vote to qualify for parliamentary seats.

Despite the large number of Muslims in Indonesia, not all voted for Islamic parties.[3] To be sure, although the non-Islamic parties are mostly led by Muslims, their goals are not to pursue shariah laws or an Islamic state. In 2019, the total number of votes gained by Islamic parties was 30.0 percent, which showed a slight drop from the 2014 figure of 31.4 percent.

Taking NU supporters as a case in point, most NU members preferred to vote for non-Islamic parties. This is surprising, as NU members constitute one of Indonesia’s biggest voter groups, and political parties tend to compete for their support. One could assume that a majority of NU members would vote for PKB, as it is a political party formally and ideologically affiliated with NU. A survey, however, reveals a different situation. More importantly, under Yahya Staquf’s current chairmanship, NU is strongly endeavouring to return to Khittah 26, which underlines the neutrality of NU in practical politics. In addition, NU’s members have been divided in their support of parties and presidential candidates.

Compared to NU, Muhammadiyah members show a different political attitude and orientation. NU leaders are bolder when expressing their political interests than Muhammadiyah members. The same situation can said concerning political affiliation. The NU leadership is open about expressing the organisation’s relationship with the PKB, and stating that the PKB is a party for NU members. Muhammadiyah, on the other hand, describes its relationship with PAN not as organisational, but as cultural. However, despite these two differring stances, both failed to secure support. Interestingly, Partai Ummat could only gain less than one percent of the popular vote, even though the founder of the party was Amien Rais, a veteran and Muhammadiyah leader.

THE QUESTION OF SOLIDITY

In addition, the solidity of Islamic parties is under serious question. Although these parties adopt different orientations—broadly distinguished as traditionalist, modernist, Islamist, progressive, and humanist—they derive legitimacy through their common promotion of Islamic values and ideals. Their political posturing differs as well, as was evident in their separate preferences for presidential candidates. For example, in order to overcome the parliamentary threshold, the PPP joined Partai Demokrasi Indonesia Perjuangan (PDI-P) in promoting Ganjar Pranowo and Mahfud MD for president and vice-president. Meanwhile, PKB and PKS endorsed Anies Baswedan and Muhaimin Iskandar as their favoured candidates. Muhaimin is incidentally a popular NU member who has a solid grassroots base in Islamic boarding schools and among traditionalist clerics (kiai).