EXECUTIVE SUMMARY

- The establishment of a Comprehensive Strategic Partnership (CSP) between ASEAN and Japan during the 50th anniversary of their partnership in September 2023 reaffirms Japan’s role as a trusted partner in Southeast Asia.

- Among ASEAN dialogue partners, Japan has been recognised as a “courteous power” that aligns well with Southeast Asian cultural norms and values. Beyond that, Japan has emerged as the most trusted and strategically relevant middle power to ASEAN in the 2024 State of Southeast Asia survey.

- Japan’s trusted status has enabled it to play a greater security role in the region, including through the new Official Security Assistance (OSA) introduced in 2023 to strengthen the security capabilities of like-minded regional countries.

- Japan’s engagement in the “Free and Open Indo-Pacific” strategy and its active role in various minilateral configurations demonstrate its strategic intent not only to foster a rules-based international order but also to enhance interoperability among regional militaries.

- Japan has recently enhanced its alliance with the United States and deepened collaborations with the Philippines, Australia, and the UK, effectively transforming the traditional “Hub and Spokes” framework into a robust network of aligned partners. This strategic evolution positions Japan to effectively bridge QUAD and ASEAN nations, facilitating the creation of a comprehensive regional security network.

* William Choong is Senior Fellow at the Regional Strategic and Political Studies Programme and Managing Editor of Fulcrum, and Joanne Lin is Associate Senior Fellow at the ASEAN Studies Centre at ISEAS – Yusof Ishak Institute.

ISEAS Perspective 2024/54, 18 July 2024

INTRODUCTION

ASEAN and Japan celebrated five decades of partnership in a Commemorative Summit in December 2023,[1] with the theme “Trusted Partners”. This aptly encapsulated a relationship built on Japan’s respectful diplomacy and ASEAN’s preference for mutual respect and shared values. Amidst the diverse challenges and opportunities in the region, Japan’s role as a trusted partner remains pivotal in shaping regional partnerships across Southeast Asia. The establishment of the Comprehensive Strategic Partnership (CSP) between ASEAN and Japan in 2023[2] underscores this strategic role.

Among ASEAN’s dialogue partners, Japan has distinguished itself as a “courteous power”[3] that aligns well with the cultural norms and values of Southeast Asian countries. Beyond its status as one of the region’s top economic, security and diplomatic partners,[4]Japan has earned the reputation of being the most relied-upon partner in the region.

Japan’s reputation in the region was reaffirmed in the State of Southeast Asia 2024 Survey,[5] where it not only maintained its position as the most trusted power but also emerged as the most strategically relevant middle power to ASEAN. While other middle powers such as Australia, the EU, India and the United Kingdom (UK) experienced a decrease in their perceived influence, Japan saw a doubling of its perceived political and strategic influence in Southeast Asia.

This Perspective delves into Japan’s status as a beacon of trust and growing influence in the broader regional multilateral framework. It is argued that Japan can leverage its stock of trust in Southeast Asia to play a bigger security role in the region. Japan’s enduring role as an all-weather friend to Southeast Asia[6] over the past five decades is reaffirmed in the survey.[7] The report continues to underscore the region’s confidence in Japan as the most trusted among five key powers, including the US, EU, China and India. When asked if Japan will “do the right thing” to contribute to global peace, security, prosperity and governance, the majority of respondents (58.9%) expressed confidence, a 4.4% increase from 2023.

Trust and Distrust Rankings of Major Powers

Source: State of Southeast Asia 2024 Survey

Among those who trust Japan, the largest group of respondents (36.5%) believe Japan is a responsible stakeholder that respects and champions international law. The second biggest reason for trust in Japan (27.7%) is its vast economic resources and its political will to provide global leadership. Approximately one-fifth of respondents (21.1%) trust Japan because they admire its civilisation and culture.

In the ranking of dialogue partners by strategic relevance to the region, Japan is the frontrunner among all the middle powers, behind only China and the US. Japan surpasses all other middle powers including the EU, South Korea, UK, Australia, Russia, India, Canada and New Zealand.

Dialogue Partners’ Strategic Relevance to ASEAN

Source: State of Southeast Asia 2024 Survey

Southeast Asian perception of Japan’s growing influence in the region is also evident in other survey responses. When asked which country is the most influential political-strategic power in the region, the number of respondents ranking Japan at the top nearly doubled from 1.9% last year to 3.7% this year. Although Japan ranks far behind China, US and ASEAN, its perceived growing influence sets it apart from other middle powers like Australia, the EU, India, and the UK, which witnessed a decline.

GROWING SECURITY ROLE IN SOUTHEAST ASIA

Southeast Asians’ trust in Japan has been conducive for Tokyo to play a bigger security role in the region. Since the 1990s, Japan has shouldered increased responsibility for maintaining security in the Asia-Pacific region.[8] During the tenures of Prime Minister Shinzo Abe (2007-2008, 2012-2020), Japan assumed a more assertive stance in both military and diplomatic spheres, largely driven by the resurgence of China.[9]

According to Abe, Japan would make a “proactive contribution to the peace”. To this end, Japan has demonstrated its resolve to build a regional security framework, based on shared principles of international law, no recourse to the use of force, and a rules-based order in both words and deeds. In 2016, Abe introduced the concept of a “Free and Open Indo-Pacific” (FOIP), aiming to capitalise on emerging opportunities and challenges across Asia and Africa. This vision is rooted in a commitment to a rules-based international order, peace, stability and economic prosperity.[10] Further refining this vision, Japan unveiled its “New Plan for a FOIP” in March 2023, acknowledging evolving global dynamics, including the rise of emerging and developing countries as well as pressing global challenges such as climate change and technology advancements.[11]]

In April 2023, Japan introduced the Official Security Assistance (OSA) programme,[12] which provides material equipment and infrastructure assistance to meet the security needs of recipient countries especially in Southeast Asia and South Asia.[13] The defence equipment provided under the OSA is limited to areas such as rescue, transport, warning, surveillance and minesweeping.[14] Japan’s rationale for the OSA was straightforward: to strengthen the security of like-minded states by improving their “deterrence capacities”, particularly in the face of “China’s growing attempts to unilaterally change the status quo by force”.[15] This serves to bolster the security capabilities of ASEAN countries, including by provision of radars and satellite systems, and reinforces Japan’s strategic engagement with the region, representing a tangible demonstration of Japan’s commitment to regional security.

The OSA is a continuation of a long-standing trend whereby Japan sought to bolster the security capacities of like-minded regional countries. While Japan’s Official Development Assistance (ODA) can only be used for social and economic development, Japan used a “sleight of hand” to send vessels, aircraft and radar systems to help Southeast Asian claimant states in the South China Sea bolster their maritime capabilities.[16] In 2013, Japan delivered 10 multi-role patrol vessels to the Philippines Coast Guard, and dispatched another two patrol boats in 2022. Tokyo has dispatched six second-hand fishery patrol ships to Vietnam. Another six will be sent by 2025.

In April 2024, Japan upgraded its alliance with the US – arguably the biggest elevation of the alliance since 1951. For the first time, the two militaries would be put under the command of a US four-star general, thus resembling the US-South Korea alliance setup, which is structured under an expeditious “fight tonight” deterrent posture.[17] The two allies plan to enable “seamless integration of operations and capabilities for interoperability.” Speaking in April 2024, Joe Biden and Fumio Kishida singled out China, saying the two allies would “respond to challenges by China through close coordination”.[18]

Within the same week, Japan and the US also incorporated the Philippines into a first-ever trilateral arrangement, which, according to Kishida would “bolster a free and open international order based on the rule of law”. President Biden reaffirmed US defence commitments to Tokyo and Manila – a clear signal to China, which had been involved in an altercation with Philippine forces in the South China Sea.[19] While Manila and Tokyo are not formal military allies with each other, the institutional linkages between the US, Japan and the Philippines are expected to grow. This would serve as a deterrent to assertive Chinese actions in disputed areas such as the South China Sea.[20]

At the same set of meetings, President Biden and Prime Minister Kishida also announced that Japan will join the second pillar of the Australia-United Kingdom-US (AUKUS) trilateral security arrangement. The second pillar would involve the development of advanced capabilities such as cyber assets, artificial intelligence and quantum capabilities.[21]The US and Japan also announced a regular series of US-Japan-UK exercises, which are slated to begin in 2025.

This underscores the thickening web of US allies and like-minded partners to uphold the regional order. Japan is already emerging as a key player in emerging minilateral arrangements, involving US allies and like-minded partners. In August 2023, the leaders of Japan, South Korea and the US inaugurated a new trilateral partnership, which would enable the three countries to consult and coordinate, on an annual basis, at various levels of their governments concerning common security and other related challenges.[22] A new multi-domain exercise, to be held annually, is also in the planning stages.[23]

Japan is also playing a role in other minilaterals. In early May, the defence ministers of Australia, Japan, the Philippines and the US met at the US Indo-Pacific Command headquarters in Hawaii to affirm their shared vision for a “free, open secure and prosperous Indo-Pacific” The meeting was apposite, given that both the US and the Philippines had just finished their annual US-Philippine Balikatan exercises (with Japan and Australia as observers), which are aimed at deterring China in the Taiwan Strait and the South China Sea.[24] In Hawaii, the defence ministers of Australia, Japan and the US also met for the 13th time to deepen cooperation to promote regional security. They announced additional trilateral exercises, such as F-35 training in the three countries, and the conduct of a first-ever combined live-fire air and missile defence exercise in 2027.

WHEN A SPOKE BECOMES A HUB

The trifecta of Southeast Asia’s growing trust in Japan, Tokyo’s willingness and ability to play an increased security role, and the thickening of a minilateral security network in the face of growing Chinese assertiveness puts Japan in a position to enhance defence cooperation with ASEAN, and also to integrate individual Southeast Asian countries into a framework involving some (or all) members of the Quadrilateral Security Dialogue (Quad).

Defence Cooperation with ASEAN

Japan already plays an active role in the ASEAN Defence Ministers’ Meeting Plus (ADMM-Plus), which spans various domains including humanitarian assistance and disaster relief, maritime security, military medicine, counterterrorism, peacekeeping operations, and cybersecurity, and has been positively received by the region.[25] In November 2023, Japan introduced a new Japan-ASEAN Ministerial Initiative for Enhanced Defense Cooperation (JASMINE).[26] JASMINE seeks to elevate ASEAN-Japan defence cooperation amid a dynamic security landscape by focusing on four key aspects, namely: (i) ensuring a security environment that does not allow unilateral attempts to change the status quo by force or coercion; (ii) expanding ASEAN-Japan defence cooperation; (iii) pursuing further friendship and opportunities between ASEAN-Japan defence officials; and (iv) supporting defence cooperation between ASEAN, Japan and the Pacific Island countries. JASMINE mirrors Japan’s vision as laid out in Japan’s Vientiane Vision in 2016. Tokyo said it wanted practical defence cooperation with ASEAN countries based on capacity building, the transfer of equipment, and joint participation in exercises.

Maritime security has emerged as a central focus for Japan, driven by escalating concerns over China’s naval activities.[27] In this context, Japan can serve as a bridge to facilitate ASEAN’s utilisation of the Quad’s Indo-Pacific Partnership for Maritime Domain Awareness,[28] leveraging innovative technology to provide real-time information on maritime activities. Collaboration in this regard will be instrumental in combating illegal, unreported, and unregulated (IUU) fishing and addressing humanitarian crises. Coordination with existing maritime centers in the region, such as the Information Fusion Centre in Singapore and the Thai Maritime Enforcement Coordinating Centre, will enhance the effectiveness of such endeavours.

Furthermore, Japan should prioritise providing regular updates to ASEAN on developments in the Indo-Pacific region, particularly regarding minilateral initiatives like the Quad and other trilateral groupings. These updates could be shared on the sidelines of events such as the ADMM-Plus or security forums like the Shangri-La Dialogue in Singapore, fostering greater trust and confidence-building between ASEAN and Japan. Such dialogues will not only enhance functional cooperation but also facilitate a clearer articulation of their respective strategic roles in the region.[29]

Quad-lite Minilaterals

By virtue of its deep linkages with the US and its San Francisco alliance network and growing defence connections with ASEAN countries, Japan is in a strategic position to link the Quad and ASEAN countries into a wider security network. Broadly speaking, the Quad and ASEAN share a common goal of ensuring regional stability and security, as well as common principles, such as the promotion of an open, inclusive and rules-based regional architecture. The point of divergence lies in what is perceived to be the Quad’s potential to undermine the centrality of ASEAN, and the consequent effects of ASEAN or its member countries working closer with the Quad (i.e. China’s opposition to such activities, given Sino-US rivalry and competition for power and influence in the Indo-Pacific). For many ASEAN countries, Quad membership is out of the question. That said, however, many Southeast Asians have become increasingly receptive to working with Quad countries to strengthen regional stability. In the 2024 State of Southeast Asia Survey, 40.9% of respondents deemed that the Quad would be beneficial to the region — up from 31% in 2023.[30]

The Quad’s ‘flexible’ and ‘nimble’ character can be expressed in what Hoang and Choong term as “Quad-lite” configurations among members of the Quad, as well as between Quad members and Southeast Asian countries. While such Quad-lite collaborations do not carry the Quad “brand” (and thus do not heighten Chinese perceptions of threat), they provide building blocks for bolstering strategic coherence and interoperability among members.[31] This thickening web includes defence and security cooperation, but also other functional domains such as economics, supply chains, and technologies.[32]

In August 2023, navies from Australia, Japan, the Philippines, and the US conducted a multilateral exercise in the South China Sea. This included the helicopter destroyer JS Izumo and destroyer JS Samidare, the US Navy Littoral Combat Ship USS Mobile and the Royal Australian Navy amphibious assault ship Canberra and frigate HMAS Anzac.[33] In April 2024, the four countries carried out joint air and naval drills, again in the South China Sea.[34] A joint statement issued by the Defence Chiefs of the four countries highlighted their “collective commitment to strengthen regional and international cooperation in support of a free and open Indo-Pacific”, and to stand with all countries “in safeguarding international order based on the rule of law”.[35]

In August 2023, the Talisman Sabre exercises involved not just Australian and American soldiers, but also soldiers, marines and aviators from Japan, South Korea and the UK. Military personnel from the Philippines, Singapore and Thailand attended as observers.[36] In September 2023, Singapore and Japan were part of a large-scale Super Garuda Shield exercise carried out by Indonesia and the US. Brunei, Malaysia and the Philippines participated as observers.[37]

Such Quad-lite interactions are not restricted to the defence/security domain. Australia, Japan and the US have offered their support for clean energy and decarbonisation projects in Vietnam. The US-Japan Mekong Power Partnership, which seeks to facilitate clean energy deployment and electrical connectivity, involves Cambodia, Laos, Thailand and Vietnam.[38] The US-led Indo-Pacific Economic Framework comprises all four Quad countries and seven Southeast Asian countries.

These working Quad-lite arrangements do not constitute an overly anti-China defence network, but this network can serve as a potential deterrent to assertive Chinese behaviour. It also means Southeast Asian countries can pursue flexible and timely arrangements with the US and its allies in the pursuit of their national interests and regional stability. The fact that Japan takes a more nuanced approach to China helps it gain traction in the region. As opposed to the US, which at times has used megaphone diplomacy to castigate China, Japan tends to take a more low-key approach, engaging with China in the realm of economics and working with Beijing even in more sensitive political and security matters. In 2018, for example, Mr Abe forged 52 memorandums of understanding with China to facilitate bilateral cooperation in third-country markets. In May 2024, there was a trilateral summit involving China, South Korea Japan. The summit discussed economic issues, as well as regional and global issues such as the Korean peninsula, the war in Ukraine and war between Israel and Hamas in the Gaza Strip.

Given Japan’s thickening linkages with the US and within the Quad, its deep relationships with Southeast Asian countries and their high level of trust in Tokyo, Japan is best placed to act as a bridge between the Quad and ASEAN countries in defence of the regional order. Going forward, Japan can encourage Southeast Asian countries to participate in military exercises involving some, if not all, Quad member countries. This could involve repeated and scheduled participation of Southeast Asian countries in the aforementioned exercises, namely, Garuda Shield, Talisman Sabre and even future iterations of the August 2023 military exercises involving Australia, Japan, the Philippines and the US in the South China Sea. In addition, Japan can consider involving more Southeast Asian countries in its Indo-Pacific Endeavour series of annual naval deployments involving its light carriers and escorting destroyers. These deployments typically involve other Quad countries. The 2022 and 2023 editions saw two ASEAN countries taking part,[39] while 2019 had seen Japanese interactions with five ASEAN countries, namely Brunei, Malaysia, the Philippines, Singapore, and Vietnam.[40]

Japan’s involvement in such Quad-lite arrangements would act as an incentive for Southeast Asian countries to do likewise. This would be beneficial to the regional order on two counts. First, the sustained participation of ASEAN countries in Quad-lite exercises will help to form patterns of cooperative norms and habits between Quad nations and Southeast Asian countries, and thus increase interoperability and coordination for future contingencies. Second, the participation of ASEAN countries in such a Quad-lite network could potentially deter Chinese behaviour that may upset the regional status quo. China has taken notice of such thickening linkages between Quad countries and ASEAN states, stressing that it opposed the “practice of bloc parties” by relevant countries.[xli] Put differently, China is keenly aware of such arrangements, and they could have some deterrent value vis-à-vis assertive Chinese behaviour.

CONCLUSION

Japan is in an advantageous position to link up the Quad and various Southeast Asian countries. By leveraging on its long-standing trust capital in Southeast Asia and its linkages to minilaterals such as the Quad, Japan can help to build a sustainable regional order based on shared principles that deter potential aggressors. In other words, the “courteous power” can bare some teeth in the pursuit of regional stability. To paraphrase Ciorciari and Tsutsui, the “courteous power” can facilitate through its growing strategic weight rather than a strong fist to nudge Southeast Asian countries towards the path Japan wants them to take – for the sake of regional security.

ENDNOTES

For endnotes, please refer to the original pdf document.

| ISEAS Perspective is published electronically by: ISEAS – Yusof Ishak Institute 30 Heng Mui Keng Terrace Singapore 119614 Main Tel: (65) 6778 0955 Main Fax: (65) 6778 1735 Get Involved with ISEAS. Please click here: /support/get-involved-with-iseas/ | ISEAS – Yusof Ishak Institute accepts no responsibility for facts presented and views expressed. Responsibility rests exclusively with the individual author or authors. No part of this publication may be reproduced in any form without permission. © Copyright is held by the author or authors of each article. | Editorial Chairman: Choi Shing Kwok Editorial Advisor: Tan Chin Tiong Editorial Committee: Terence Chong, Cassey Lee, Norshahril Saat, and Hoang Thi Ha Managing Editor: Ooi Kee Beng Editors: William Choong, Lee Poh Onn, Lee Sue-Ann, and Ng Kah Meng Comments are welcome and may be sent to the author(s). |

EXECUTIVE SUMMARY

- The European Union (EU) consistently occupies the top spot in Southeast Asia as the preferred and trusted “third party” in hedging against the uncertainties of US-China rivalry and in commitment to “doing the right thing” in the wider interests of the global community.

- The EU’s strong economic and normative presence in the region is recognised. It is ASEAN’s third largest trading partner and source of FDI. Brussels is also recognised for its strong values regarding multilateralism and its commitment to a rules-based order, forming the cornerstone of the ASEAN-EU strategic partnership.

- However, trust in the EU amongst Southeast Asians is at its lowest level since it launched its Indo-Pacific Strategy in 2021. This is due, in part, to the preoccupation of its member states with domestic and European issues such as Ukraine, as well as unresolved disputes and trade concerns with Southeast Asian countries over palm oil and the EU’s carbon policies. Concerns about human rights violations, democratic backsliding and governance deficit happening in several ASEAN countries continue to underscore the inherent tensions between the EU’s normative aspiration and its pragmatic engagements in the region.

- The EU has room for improvement if it wishes to make good on its Indo-Pacific strategy. It needs to recognise the practical limitations that Southeast Asian countries have in complying with its regulations. It can facilitate economic development across the region through capacity-building programmes aimed at harmonising regulatory standards. It should also focus on its strengths in areas of non-traditional security rather than traditional military domains. Most importantly, the EU should recalibrate its balancing of principles and pragmatism to not only advance mutual interests but also cement its relevance in Southeast Asia.

* Eugene R.L. Tan is a Research Officer with the Regional Strategic and Political Studies Programme at ISEAS – Yusof Ishak Institute; and Joanne Lin is Co-coordinator and Associate Senior Fellow at the ASEAN Studies Centre at ISEAS – Yusof Ishak Institute.

ISEAS Perspective 2024/41, 5 June 2024

INTRODUCTION

The European Union’s (EU) role in Southeast Asia continues to be acknowledged, particularly amid the escalating competition between the US and China. As a longstanding dialogue partner of ASEAN since 1977, the EU has emerged as a major development partner for ASEAN and stands as the region’s third largest trading partner and foreign direct investment (FDI) source.[1] As its relations with ASEAN have been elevated to a strategic level since 2020, the EU has extended its influence beyond economic and normative domains.

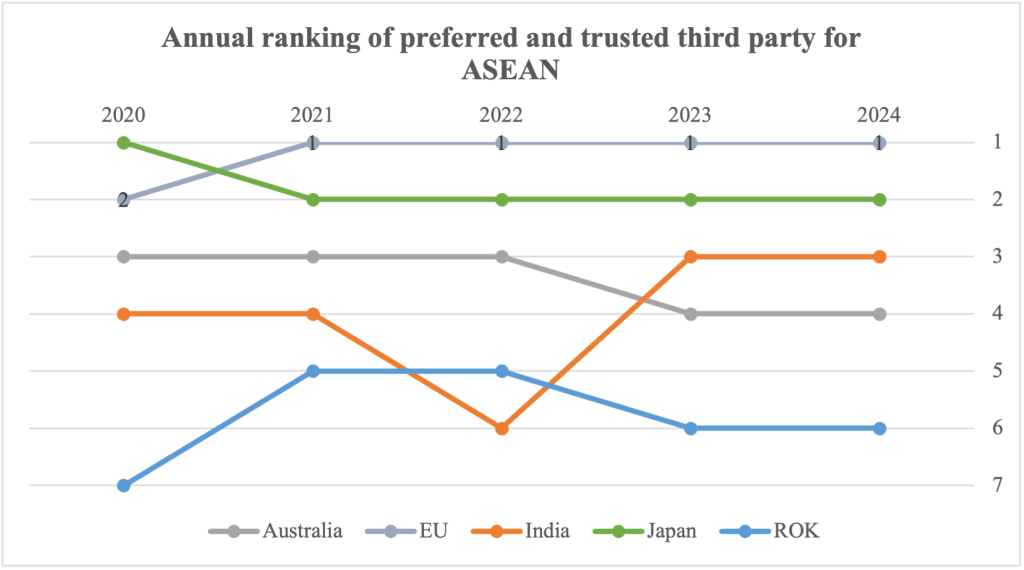

There is plenty of evidence underscoring the EU’s consistent image as a reliable and pivotal actor in Southeast Asia. In the State of Southeast Asia surveys,[2] the EU has, since 2021, occupied the top spot as the region’s preferred and trusted “third party” in hedging against the uncertainties of the US-China strategic rivalry (see Figure 1). The EU also remains a trusted global actor committed to “doing the right thing” in the wider interests of the global community, according to the same survey. Notably, in the 2024 survey,[3] the EU emerged as the fourth most strategically relevant dialogue partner, among eleven countries, positioning it closely behind China, the US, and Japan (see Table 1).

Figure 1: Annual ranking of preferred and trusted third-party for ASEAN

Source: State of Southeast Asia Surveys[4]

Table 1: Dialogue Partners ranked in order of strategic relevance in 2024

| Rank | Dialogue Partner | Mean Score |

| 1 | China | 8.98 |

| 2 | US | 8.79 |

| 3 | Japan | 7.48 |

| 4 | EU | 6.38 |

| 5 | ROK | 5.71 |

| 6 | UK | 5.52 |

| 7 | Australia | 5.51 |

| 8 | Russia | 5.08 |

| 9 | India | 5.04 |

| 10 | Canada | 3.81 |

| 11 | NZ | 3.70 |

Source: 2024 State of Southeast Asia Survey

The EU seems poised to strengthen its role as a middle power in an increasingly strategic region of geopolitical contestation. In 2021, the European Council launched its Strategy for Cooperation in the Indo-Pacific in an attempt to strengthen its access to regional markets, strengthen its supply chain and uphold the tenets of a rules-based international order as an alternative to China’s Belt and Road Initiative (BRI).[5] Despite the EU’s ambition in the Indo-Pacific, it faces certain constraints. The ongoing war on its Eastern flank and serious concern about its ability to fund its own defence amid wavering US support cast doubt on the EU’s commitment to Southeast Asia. Furthermore, echoes of disunity have been getting louder, not only from smaller member states like Hungary,[6] but also between larger member states like France and Germany; notably, the lack of a “common front” in their bilateral relationships with China[7] is indicative of wider divergences between the pair of countries leading the EU’s Indo-Pacific approach. Considering these challenges, German Chancellor Olaf Scholz characterised Europe’s trajectory in the last two years as a “Zeitenwende” (i.e. historic turning point), prompting an inward focus on addressing domestic capacity and challenges.

The perception of a disunited and conflict-ridden Europe can have ripple effects in Southeast Asia. Concurrently, persistent concerns about human rights violations, democratic backsliding and governance deficit in certain ASEAN countries continue to underscore the inherent tensions between the EU’s normative aspiration and its pragmatic engagements in the region. This article examines the EU’s role as a resilient and reliable middle power in shaping Southeast Asia’s future, while exploring avenues for the EU to play a more influential role in the region.

EU’S ECONOMIC AND NORMATIVE POWER IN SOUTHEAST ASIA

Despite the absence of a Free Trade Agreement (FTA) with ASEAN, the EU maintains a robust economic presence in the region. As ASEAN’s third largest trading partner (trailing only behind China and the US), ASEAN-EU trade reached US$ 295.2 billion in 2022, marking a significant 9.6% year-on-year growth.[8] Additionally, the EU maintains its economic foothold as the third-largest source of FDI into ASEAN, with a substantive inflow of US$24 billion in 2022.[9] According to data from ASEAN Investment Reports[10] from the same period, EU member states such as France, Germany and the Netherlands were among ASEAN’s top sources of FDI.

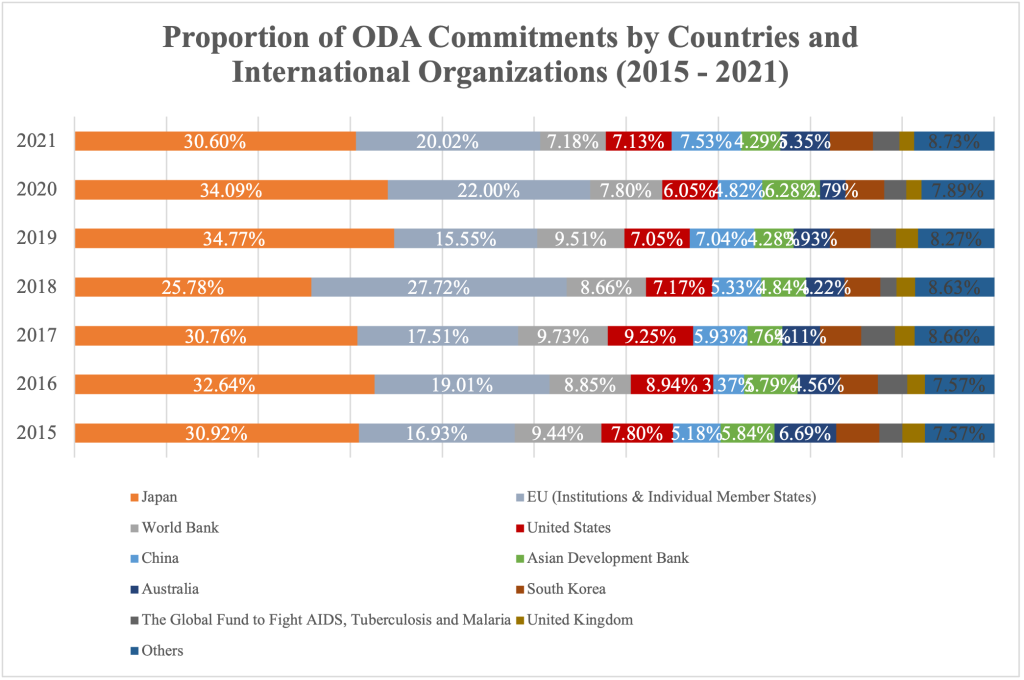

Moreover, EU institutions, alongside their member states were the second largest provider of official development assistance (ODA) to the region between 2015 and 2021 (see Figure 2), signifying the EU’s multifaceted economic commitment to the region. The EU has also been viewed as the fourth most influential economic power in the region in the State of Southeast Asia from 2019 – 2024, ahead of middle powers such as Australia, India, South Korea, and the United Kingdom (UK).

Figure 2: Proportion of ODA Commitments by Countries and International Organizations (2015 – 2021)

Source: Lowy Institute Southeast Asia Aid Map[11]

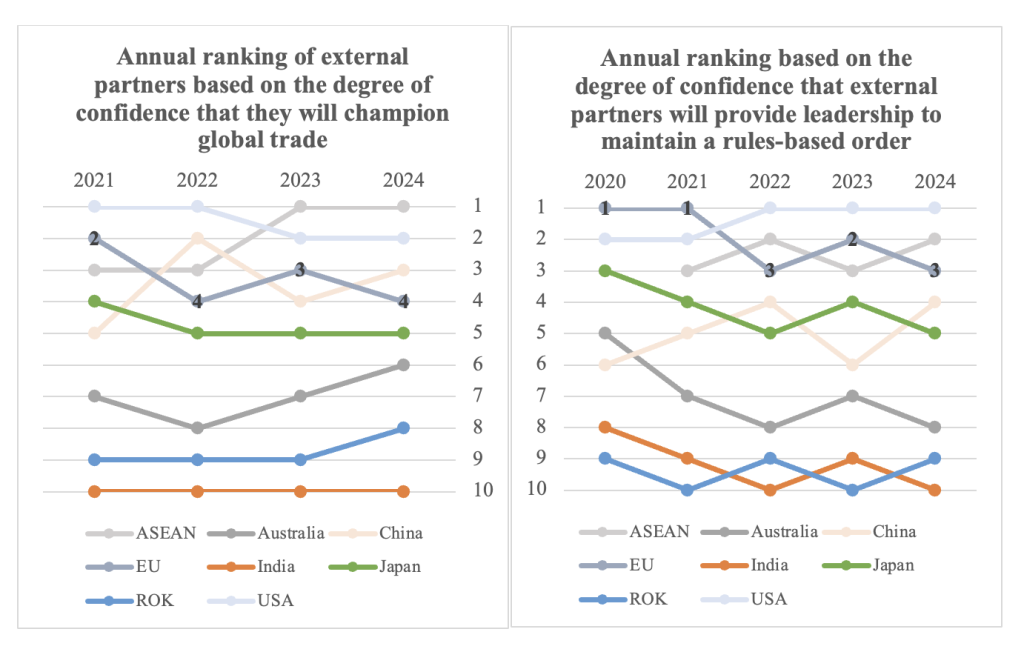

Beyond its economic clout, Brussels is also recognised as a strong normative actor in the region. As part of its Strategy for Cooperation in the Indo-Pacific,[12] the EU has sought to cooperate with like-minded countries to set standards and promote good regulatory practices.[13] It indicated its ambition to promote an open and rules-based regional security architecture and safeguard freedom of navigation in the region through capacity-building initiatives. As such, shared values, including multilateralism and commitment to a rules-based order, remain the cornerstone of the ASEAN-EU strategic partnership.[14] This has translated into greater confidence in Brussels’ capacity to champion global free trade and maintain a rules-based order, with the EU ranking above other middle powers in the region across both measures (see Figures 3 and 4).

Figures 3 and 4: Annual ranking of external partners based on the degree of confidence that they will champion global trade or provide leadership to maintain a rules-based order

Source: State of Southeast Asia Surveys[15]

“PROTECTIONIST” BRUSSELS AND DIVERGING VALUES

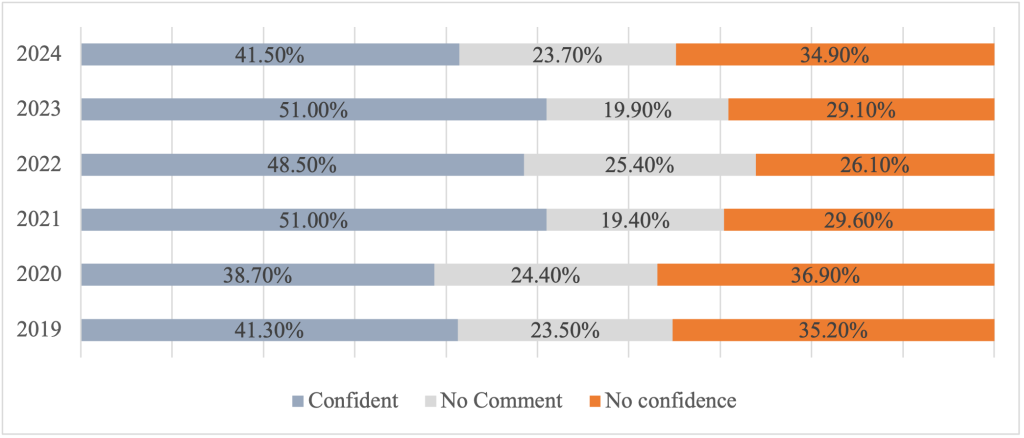

While the EU’s influence and standing appear relatively strong, its engagement with the region is not without challenges. Persistent economic issues, such as unresolved disputes over palm oil and regional anxiety regarding the EU’s carbon policies, present ongoing obstacles. Furthermore, regional, and global geopolitical challenges such as the Myanmar crisis and the Israel-Hamas war complicate the EU’s engagements with some ASEAN member states, particularly Muslim-majority countries. As such, trust levels in the EU amongst Southeast Asians are at their lowest since it launched its Indo-Pacific Strategy in 2021 (see Figure 5).

Figure 5: Confidence in the EU to “do the right thing” to contribute to global peace, security, prosperity, and governance among Southeast Asian Respondents

Source: State of Southeast Asia Surveys[16]

A growing source of distrust are the EU’s ongoing trade disputes with Indonesia and Malaysia over protectionist practices. The EU formally challenged Indonesia’s “unlawful export restrictions” on nickel and iron ores at the WTO.[17] The WTO has ruled in favour of the EU since October 2022, and the ban remains in effect while Indonesia appeals the decision.[18] Concurrently, the EU’s implementation of the Renewable Energy Directive (RED II)[19] to phase out the import of palm oil by 2030 has sparked contention. As the largest producers of palm oil globally, both Indonesia and Malaysia have lodged cases with the WTO,[20] arguing that the EU had similarly infringed on the rules of international trade. Similar concerns have been voiced by rubber producers across the region in response to the EU’s regulation on deforestation-free products, which entered into force in June 2023.[21] Producers from Indonesia,[22] Malaysia, Thailand and Cambodia have expressed concern that Brussels’ “unilateral and unrealistic”[23] action would disproportionately disadvantage smaller farmers over large corporations.

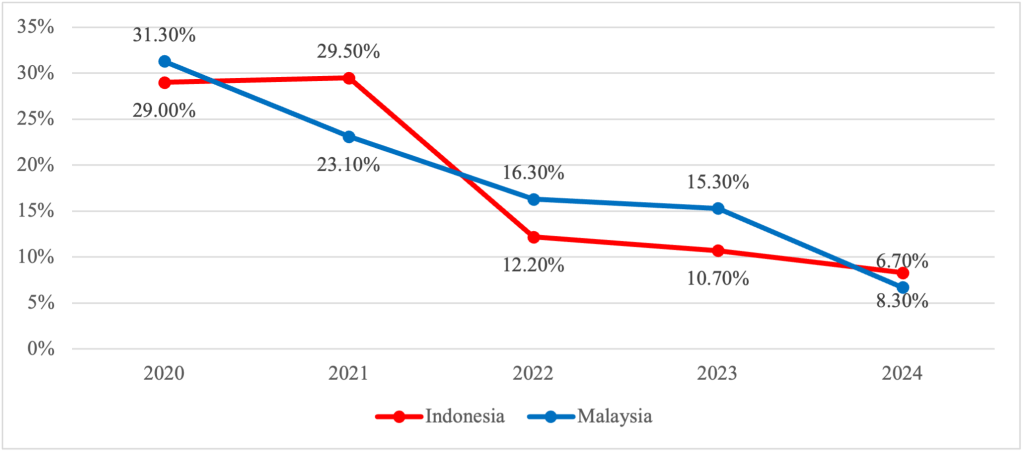

As such, the perceived disjuncture between Brussels’ opposition to Indonesian critical mineral protectionism and its own exercise of “protectionist”[24] and “discriminatory”[25] practices, such as favouring European biofuels like rapeseed oil,[26] invites accusations of hypocrisy and double standards. Moreover, the EU’s Carbon Border Adjustment Mechanism (CBAM) has been criticised as a protectionist tool benefiting EU companies at the expense of Southeast Asian competitors.[27] These measures have incurred reputational costs for the EU in the region,[28] as reflected in the decline in confidence in the EU to champion the global free trade agenda, between 2020 and 2024 among Indonesian and Malaysian respondents (see Figure 6).

Figure 6: Confidence among Malaysian and Indonesian Respondents in the EU to “do the right thing” to contribute to global peace, security, prosperity, and governance

Source: State of Southeast Asia Surveys[29]

These trade disputes with Indonesia and Malaysia have impeded progress in an already tricky free trade agreement (FTA) negotiation process for the EU. For instance, despite engaging in 16 rounds of talks since 2016, the EU and Indonesia have made little headway, with no resolution in sight.[30] Similarly, the EU and Malaysia have suspended talks on their bilateral FTA since 2012.[31] At the regional level, the EU has only managed to put into force bilateral FTAs with two ASEAN member states – Singapore and Vietnam, with two others, namely Thailand and the Philippines, remaining under negotiation (see Annex A). This limited progress has hindered efforts to establish a wider region-to-region FTA between the EU and ASEAN, dampening regional confidence in the EU’s ability to champion the global free trade agenda over time.

On another front, the EU’s emphasis on values such as “fair trade”,[32] particularly in linking trade to democracy and other non-economic outcomes, has proven to be counterproductive and fraught with sensitivities.[33] The inherent misalignment regarding democracy is a persistent point of contention due to the diverse governance system in Southeast Asia,[34] leading ASEAN countries to consistently resist European democracy and human rights policies.[35] While it should be noted that Brussels has tamped down its proselytizing on “values”, it still holds numerous criticisms and resolutions against all ASEAN countries, including Singapore (see Annex A). Cognisant of this, the EU has struggled to prevent bilateral issues from complicating inter-regional cooperation.[36]

The increasing divergence between the worldviews of ASEAN and the EU is further exemplified by their differing responses to the war in Ukraine and the Israel-Hamas conflict. On the former, the EU has taken a firm stance against Russia’s aggression while ASEAN’s reaction has been largely ambivalent, with only Singapore imposing financial sanctions on Russia in response to its invasion of Ukraine.[37] Interestingly, the State of Southeast Asia 2024 Survey[38] highlights that economic concerns, such as the increase in energy and food prices, are prioritised by the majority in the region (68.4%). This emphasis underscores the region’s focus on immediate economic challenges over broader values such as the erosion of trust in a rules-based order and the violation of national sovereignty (14.5%).

On the Israel-Hamas conflict, there is a convergence of opinion between the EU and ASEAN on humanitarian grounds, with both parties agreeing that Israel should not be allowed to cut off humanitarian aid from the Gaza strip. Beyond this singular intersection however, opinions between the two regions diverge significantly. For the EU, the predominant position is to condemn the attacks on Israeli civilians on 7 October as “unjustifiable and inexcusable”.[39] By contrast, ASEAN member states have had a plethora of different responses to the conflict,[40] which is reflected in the ASEAN Foreign Ministers Statement.[41] While the position of some ASEAN member states, like the Philippines, may align more closely with that of the EU, others such as Malaysia and Indonesia have instead shown solidarity with the Palestinians.[42]

A UNION DIVIDED AND WEAK

Apart from trade tensions and diverging values, Southeast Asian respondents have been consistently concerned regarding the EU’s potential to be distracted by internal affairs and its perceived lack of capacity or political will to engage globally. These concerns were the two most cited reasons in the State of Southeast Survey between 2020 and 2024 for respondents to distrust Brussels (see Table 2).

Table 2: Proportion of Southeast Asian responses to the question “Why do you distrust the EU?”

| Response to “Why do you distrust the EU?” (%) | 2020 | 2021 | 2022 | 2023 | 2024 |

| The EU does not have the capacity or political will for global leadership | 33.70 | 25.90 | 26.70 | 33.40 | 28.20 |

| My country’s political culture and worldview are incompatible with The EU’s | 16.60 | 9.50 | 12.40 | 9.20 | 16.50 |

| I am concerned that The EU is distracted with its internal affairs and thus cannot focus on global concerns and issues | 35.40 | 38.70 | 30.10 | 29.40 | 28.70 |

| The EU’s stance on environment, human rights, and climate change could be used to threaten my country’s interests and sovereignty | 3.50 | 15.10 | 17.70 | 14.50 | 11.10 |

| I do not consider The EU a reliable power | 10.80 | 10.80 | 13.10 | 13.50 | 15.50 |

Source: State of Southeast Asia Surveys[43]

Indeed, realistic concerns persist regarding the EU’s ability to foster solidarity amongst its member states. Contentious disagreements within the EU over funding support to Kyiv underscores this challenge[44] Furthermore, domestic issues such as mounting dissatisfaction over the rising cost of living, agricultural protests sparked by EU’s regulations,[45] the European debt crisis and bailout negotiations[46] as well as the complexities of the EU’s policy towards Israel and Palestine[47] are just some examples of internal tensions.

Externally, the ongoing conflict in Ukraine and the escalating violence in the Middle East are expected to strain the EU’s policymaking capabilities and divert resources from its Indo-Pacific ambitions.[48] Furthermore, the EU’s overreliance on the North Atlantic Treaty Organization (NATO) for its defence raises questions about its commitment to security cooperation with Southeast Asia. With the possibility of a second Donald Trump US presidency on the cards following the upcoming US Presidential elections, EU members may face increased pressure to bolster their defence spending,[49] further complicating the EU’s strategic posture.

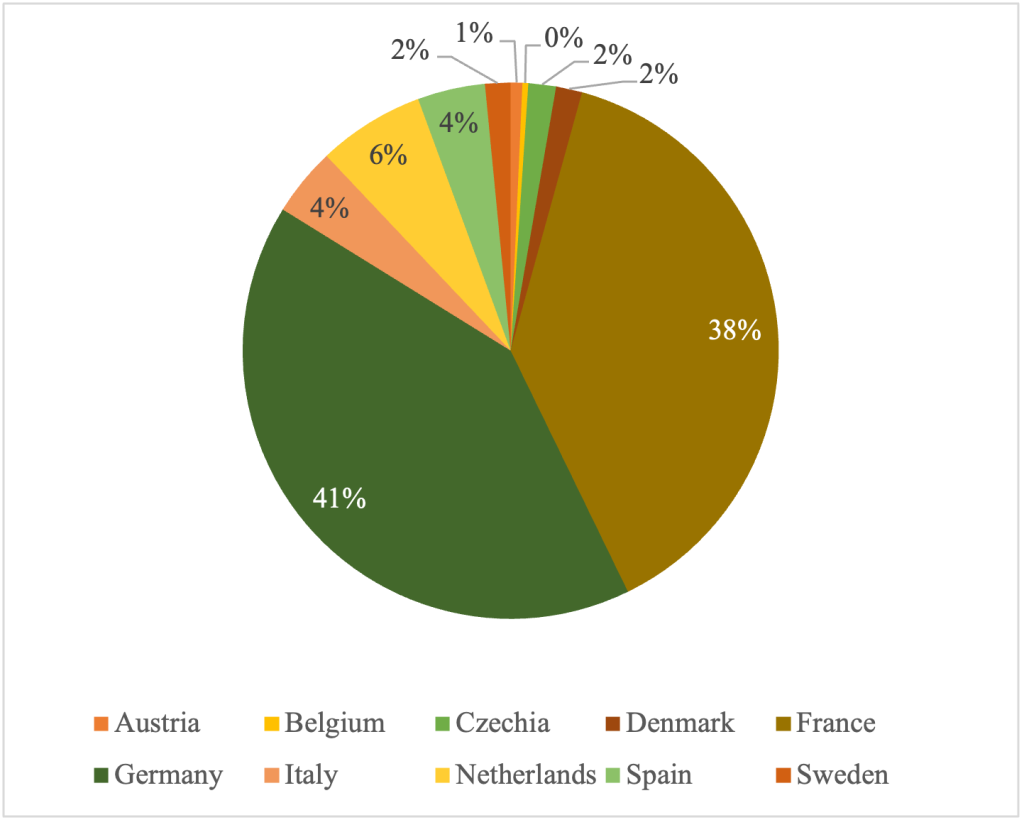

Indeed, despite its lofty ambitions to play a security role in the Indo-Pacific, the EU’s security endeavours have unfolded in a piecemeal manner that is primarily led by larger member states, with Germany and France accounting for 79% of all arms transfers from EU countries to the region between 2019 and 2023 (see Figure 7).

Figure 7: Breakdown of Arms Transfers to Southeast Asia by EU member states respectively (2019-2023

Source: Stockholm International Peace Research Institute (SIPRI) Arms Transfer Database[50]

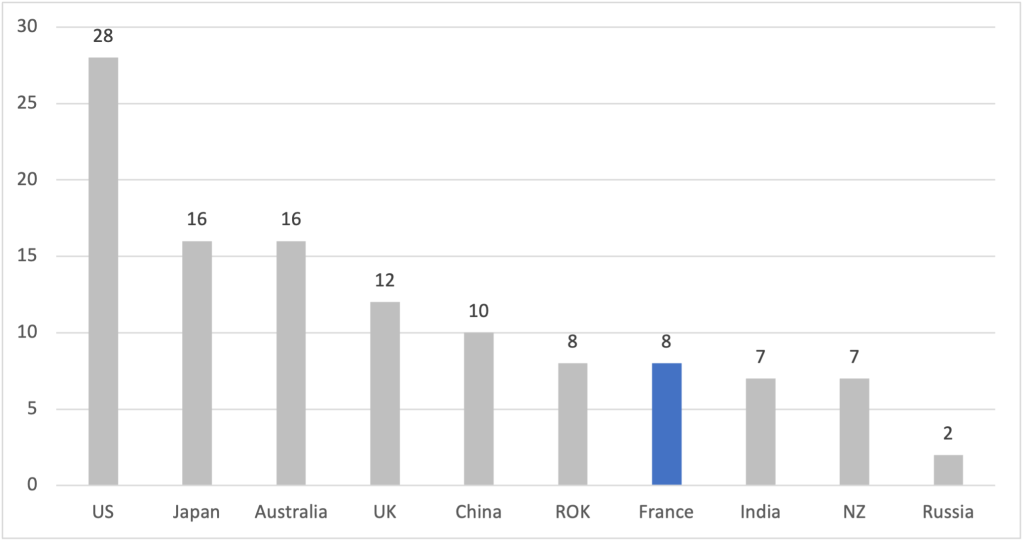

Similarly, despite its pledges to increase its naval presence in the Indo-Pacific, France remains the main driver of the EU’s naval efforts (see Figure 8). In 2023 alone, France led the EU by participating in 8 military exercises with Southeast Asian countries. However, it continues to trail middle powers in the region which have a more established naval presence, such as Australia and the United Kingdom (UK).

Figure 8: Number of Regional Military Exercises observed or participated in among external powers in 2023

Source: Data compiled by authors

STRENGTHENING EU’S RELEVANCE IN THE REGION

While the EU may face challenges in realising its security ambitions, it still holds some sway in the region and may yet find its sweet spot. Its steadfast role as a normative and economic partner has fostered trust among Southeast Asian states.

The EU has room for improvement if it wishes to make good on its Indo-Pacific strategy. Squaring away its trade disputes with countries in Southeast Asia is a tricky fruit for the EU to pick. However, the EU can recalibrate its balancing of principles and pragmatism by recognising the practical limitations that Southeast Asian countries have in complying with its regulations. Instead of expecting ASEAN to achieve EU trade standards outright, the EU can facilitate economic developments across the region through capacity-building programmes aimed at harmonising regulatory standards within ASEAN.

Rather than focusing on hard security, a domain better suited to its most capable member states,[51] the EU can focus its strengths on areas of non-traditional security. These include cybersecurity, food security, combatting Illegal, Unreported and Unregulated (IUU) fishing, climate change mitigation, sustainable development, and the regulation of emerging technologies such as AI governance and data protection.

In sum, the EU has been a steadfast partner for Southeast Asian countries and has fared well as a normative and economic power in the region. By working on its trade relations, prioritising pragmatism and focusing on areas of strength, the EU can remain a relevant and reliable middle power in Southeast Asia.

Annex A

Summary of Relations between ASEAN Member States – EU

| AMS | Key Agreements Signed with EU | Key Agreements in Progress | Bilateral Issues with the EU |

| ASEAN | EU-ASEAN Strrategic Partnership EU-ASEAN Plan of Action 2018-2022 EU-ASEAN Cooperation Agreement EU-ASEAN Comprehensive Air Transport Agreement | EU-ASEAN FTA | |

| Brunei | EU-Brunei Partnership and Cooperation Agreement (PCA) | HUMAN RIGHTS: EU Parliament condemned the entry into force of the Sharia Penal code due to human rights concerns | |

| Cambodia | EU-Cambodia 1977 Cooperation Agreement | HUMAN RIGHTS: EU Commission withdrew part of tariff preferences under Everything but Arms (EBA) scheme due to human rights issues. HUMAN RIGHTS: EU Parliament adopts resolution regarding political persecution and human rights violations | |

| Indonesia | EU-Indonesia Comprehensive Economic Partnership Agreement | BIOFUELS: Dispute over palm oil HUMAN RIGHTS & DEMOCRACY: EU Parliament “expressed concern” over proposed Indonesian criminal code | |

| Laos | EU-Laos 1997 Cooperation Agreement Everything But Arms (EBA) Trade Initiative [Not agreement] | HUMAN RIGHTS: EU notes human rights concerns on displaced people from dam construction, sexual exploitation of children HUMAN RIGHTS: EU “raised concern” about lack of progress on human rights issues | |

| Malaysia | EU-Malaysia Partnership and Cooperation Agreement (PCA) | EU-Malaysia FTA | BIOFUELS: EU Commission launched the Renewable Energy Directive which led to disputes about biofuels such as palm oil HUMAN RIGHTS & DEMOCRACY: EU Parliament has condemned the use of the death penalty, the lack of LGBTQ Rights and no freedom of speech |

| Myanmar | Everything But Arms (EBA) Trade Initiative [Not agreement] | DEMOCRACY: Sanctions and condemnations due to military coup HUMAN RIGHTS: Condemnations due to Rohingya Crisis | |

| Philippines | EU-Philippines Partnership and Cooperation Agreement (PCA) Agreement on finding a “peaceful and inclusive solution” to SCS GSP+ trade preferences scheme | EU-Philippines FTA | HUMAN RIGHTS: The Philippines “reminded” to comply with Human Rights standards as part of its commitment to the GSP+ Agreement HUMAN RIGHTS: Threatened to withdraw temporarily GSP+ Preferences (but no action yet) HUMAN RIGHTS: Strongly condemned extrajudicial killings and human rights violations in Duterte’s war on drugs |

| Singapore | EU-Singapore Partnership and Cooperation Agreement (EUSPCA) EU-Singapore Free Trade Agreement (EUSFTA) EU-Singapore Investment Protection Agreement (EUSIPA) EU-Singapore Digital Partnership (EUSDP) | HUMAN RIGHTS: EU Parliament calls for the abolition of the death penalty | |

| Thailand | EU-Thailand 1980 Framework Agreement EU-Thailand Partnership and Cooperation Agreement | EU-Thailand FTA | HUMAN RIGHTS: EU Parliament adopted “several resolutions” condemning Human Rights and migrant/labour rights violations |

| Vietnam | EU-Vietnam Partnership and Cooperation Agreement (PCA) EU-Vietnam Free Trade Agreement EU-Vietnam Investment Protection Agreement EU-Vietnam Framework Participation Agreement EU-Vietnam Sustainable Energy Transition Programme (SETP) | HUMAN RIGHTS & DEMOCRACY: EU Parliament adopted a resolution on Vietnam for unlawful arrest of human rights activists and journalists |

Source: European Parliament Fact Sheets on the European Union: Southeast Asia[52]

ENDNOTES

For endnotes, please refer to the original pdf document.

| ISEAS Perspective is published electronically by: ISEAS – Yusof Ishak Institute 30 Heng Mui Keng Terrace Singapore 119614 Main Tel: (65) 6778 0955 Main Fax: (65) 6778 1735. Get Involved with ISEAS. Please click here: /support/get-involved-with-iseas/ | ISEAS – Yusof Ishak Institute accepts no responsibility for facts presented and views expressed. Responsibility rests exclusively with the individual author or authors. No part of this publication may be reproduced in any form without permission. © Copyright is held by the author or authors of each article. | Editorial Chairman: Choi Shing Kwok Editorial Advisor: Tan Chin Tiong Editorial Committee: Terence Chong, Cassey Lee, Norshahril Saat, and Hoang Thi Ha Managing Editor: Ooi Kee Beng Editors: William Choong, Lee Poh Onn, Lee Sue-Ann, and Ng Kah Meng Comments are welcome and may be sent to the author(s). |

EXECUTIVE SUMMARY

- At the centre of the US-China trade war are the semiconductor chip and green industries.

- ASEAN is clearly benefiting from the resultant reconfiguration of the global supply chains in these two industries in terms of trade, value addition and foreign direct investment, at least in the short run. However, these benefits can be more than offset by the greater disruption to the global supply chains should US-China tensions continue to escalate.

- Its high trade reliance on China while having the US as its largest investor (by far) and key source of technology transfers puts ASEAN in an increasingly precarious situation should the US-China supply chain decoupling intensifies.

- Forcing ASEAN to choose sides – whether to be in the US or China supply chain system – will be impossible and disruptive, and ASEAN should continue to take the pragmatic approach and reject choosing sides.

* Aufa Doarest is Private Sector Specialist at the World Bank Group’s Finance, Competitiveness and Innovation and Maria Monica Wihardja is Economist and Visiting Fellow at ISEAS – Yusof Ishak Institute and Adjunct Assistant Professor at the National University of Singapore.

ISEAS Perspective 2024/35, 17 May 2024

INTRODUCTION

Interdependence within the global supply chain has been exacerbated by the growing dependence for intermediate inputs on only a few firms and a few countries (Pangestu, 2023). The semiconductor industry and the green technology industry are two examples of highly concentrated supply chains where firms from East Asia (e.g., China, Taiwan and South Korea) are now the dominant suppliers (Miller, 2022; Nguyen-Quoc, 2023).

The heightened dependence of the US on China has raised geopolitical rivalry between the two countries and driven the reconfiguration of supply chains. Countries and companies now seek to ‘decouple’, ‘diversify’ and ‘de-risk’ their supply chain configuration away from their adversaries. Consequently, supply chains in Asia are undergoing major changes.

At the country level, a number of strategies are being adopted, including re-routing trade flows through intermediary countries; home-shoring investment through investment subsidies and tax credits; and increasing self-reliance through import substitution and research and development (R&D). At the corporate level, multinational companies (MNCs) in Asia and worldwide are adapting by adopting the ‘China Plus One’ or ‘China Plus Two or Three’ model to broaden their supply base outside China while maintaining a presence in China (Nguyen-Quoc, 2023).

This essay reviews and analyses how ASEAN economies have been impacted by the changing dynamics in the global supply chain. We focus on two industries, namely the semiconductor industry and the electric vehicle (EV) industry,[1] and look at the impacts from three angles: trade, investment and R&D.

THE US INDUSTRIAL POLICY IN CHIP AND GREEN TECHNOLOGY

Since 2018, during the Trump administration, the US has been restricting the exports of “emerging and foundational technologies” to entities abroad whenever those technologies are “essential to the national security of the US” (Bradford, 2023). This started with the Export Control Reform Act of 2018 enforced through the maintenance of a Commerce Control List and a licensing system as well as a narrower export control instrument known as the Entity List. Although the idea was to restrict exports exclusively for advanced technologies that could endanger national strategic interest – dubbed as the ‘small yard, high fence’ strategy – these export restrictions were later expanded in terms of both technologies and entities. For example, in 2020, the 2018 export restrictions to ban Huawei’s access to semiconductors were extended to cover all foreign technology companies (instead of only US firms) that use US chipmaking equipment and software tools.

In August 2022, the CHIPS (Creating Helpful Incentives to Produce Semiconductors) and Science Act allocated USD280 billion to catalyse investments in domestic semiconductor R&D and manufacturing capacity. In October 2022, a set of export restrictions were issued to cut off China’s access to advanced AI chips and choke point technologies[2] (Ing and Markus, 2023). Later, these export restrictions were expanded into restrictions on direct investment (Shalal and Freifeld, 2023) and financial investment (private equity and venture capitals) (Siqi, 2024), as well as restrictions on individuals who hold US passports from working for Chinese chip companies (Lin and Hao, 2022).

In a spirit similar to the CHIPS and Science Act, in August 2022, the US also signed into law the Inflation Reduction Act (IRA) to catalyse investment in R&D and domestic manufacturing capacity in leading-edge green technologies, including carbon capture and storage as well as EV (Badlam et al, 2022b).[3] The law will direct USD400 billion into a mix of tax incentives, grants, and loan guarantees.

The concentration of green technology production and the critical minerals associated with it in China—and in a few Chinese firms—has sounded an alarm bell for the US. For example, China dominates 75 percent of Solar Photovoltaic technology and battery manufacturing compared to the small share the US has of only 5 percent in the production of both technologies (Li and Zhao, 2023). Similarly, China commands 55 percent of wind technology manufacturing.

The IRA is the US’ biggest and most significant national policy to combat climate change. However, it is unclear whether the IRA will leave any room for collaboration in low-carbon technologies where China is a major player, or lead to race-to-the-bottom protectionist industrial policies and strategic competition similar to that now found in the chip industry (Li and Zhao, 2023). Given the high concentration of green technology in China, diversification of trade sources is commendable. However, focusing on where the green technologies are built could risk slowing down the low-carbon transition in the US and globally.

THE CHALLENGES OF SUPPLY CHAIN RECONFIGURATION

At the centre of the US-China trade war and supply chain reconfiguration are chip and green technologies. Chip production-related activities, including assembling, packaging and testing, account for a significant share of the GDP and/or exports of ASEAN countries such as Malaysia, Singapore, Thailand and the Philippines (EDB, 2022a; EDB, 2022b).[4]

Supply chain reconfiguration in this context refers to aspects of production being shifted to countries or firms which are not necessarily the most competitive and efficient, due to geopolitical and national security factors. The new countries and firms may even have siloed technologies and production processes that are disconnected from others in the supply chain.

The impacts of supply chain reconfiguration on ASEAN economies can be strongly noted in three areas, namely (1) trade diversion through several intermediary countries to avoid goods flowing directly from China to the US, (2) relocation of FDI, (3) Research and Development (R&D) activities. The following sections discuss these separately.

TRADE [5]

China’s dominance as the world’s manufacturing superpower (Baldwin, 2024) is partly reflected in a significant increase in China’s export of EV (including Completely Built-Up and Completely Knocked Down cars but not parts such as batteries) and chips between 2017 and 2022. Within that period, China’s export of chips almost doubled, from USD 72 billion to USD129 billion, while China’s export of EV increased by almost 13 times, from USD2 billion to USD25 billion (Figure 1 and Figure 2).

Figure 1: China’s export and import of chips (in million USD)

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations

Figure 2: China’s export and import of EVs (in million USD)

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations

The US-China tech war, especially the escalating restrictions on China’s access to US technologies that started in 2018, are reflected in the trade in chips between the two countries in 2022. After an increasing trend since 2017, China’s import value of chip from the US declined from USD15.1 billion in 2021 accounting for 10.2 percent share of China’s total import of chips, to USD11.6 billion in 2022 accounting for 8.0 percent share (Table 1). Mirroring China’s import value decline is US’ export value decline of chips to China.

Table 1: US’ export of chips to China and China’s import of chips from the US

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations.

Note: There are multiple reasons for discrepancies in exports and imports data so that they don’t always mirror each other. See: https://wits.worldbank.org/wits/wits/witshelp/content/data_retrieval/T/Intro/B2.Imports_Exports_and_Mirror.htm

The US decision to diversify its trading partners and move away from China affects international trade in chips. First, China’s chips export destination pattern has slightly shifted. The share of China’s chips export to the US dropped from 19 percent in 2018 to 11 percent in 2022. At the same time, the share of China’s chips export to ASEAN countries increased slightly from 18 percent in 2018 to 20 percent in 2022 (Table 2). While the changes in the destination pattern may be due to lack of domestic demand in the US, the positive trend of US import of chips, increasing from USD79.7 billion in 2018 to USD87.2 billion in 2022, reveals that US domestic demand has actually gotten stronger. It is predicted that the demand for chips will continue to increase as AI, robots and EV become the new normal in people’s everyday lives.

Table 2: Chips export shares of China, ASEAN and Mexico (%)

| China’s Chips Export Share (%) | ASEAN’s Chips Export Share (%) | Mexico’s Chips Export Share (%) | |||

| China to ASEAN | China to Mexico | China to USA | ASEAN to USA | Mexico to USA | |

| 2017 | 17.4 | 1.3 | 17.9 | 12.0 | 69 |

| 2018 | 18.4 | 1.4 | 19.2 | 9.0 | 65 |

| 2019 | 19.5 | 1.3 | 16.6 | 9.8 | 58 |

| 2020 | 21.5 | 1.3 | 12.7 | 11.9 | 60 |

| 2021 | 20.2 | 1.4 | 10.4 | 11.5 | 65 |

| 2022 | 20.1 | 1.6 | 11.1 | 14.0 | 67 |

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations

Second, this export diversion is reflected in the import pattern of chips. The US import share of chips has shown an increasing reliance on ASEAN and a decreasing reliance on China (Figure 3). Both ASEAN and China accounted for 34 percent of US chips import in 2017; but while ASEAN’s share increased to 48 percent in 2022, China’s share was halved to 17 percent. Meanwhile the share of Mexico in US chips imports has barely changed while the share held by other countries has increased by 4 percentage points in the same period. This shows that ASEAN is clearly benefiting from US’ import diversion away from China.

Figure 3: US import of chips

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations

Unlike the chips trade, the trend of EV trade between the US and China continued to be robust in terms of value until 2022 but declined in terms of reliance (or share) (Table 3). The US used to account for 28.1 percent of China’s export in EVs but this fell to only 7.9 percent in 2022. At the same time, China had accounted for 52.5 percent of US’ import in EV but this declined to 12.8 percent in 2022.; ASEAN’s export of EVs has been increasingly going to the US (Table 4) while ASEAN’s import of EVs has been increasingly coming from China (Figure 4). The two-wheeler EV has been driving the increase in ASEAN’s export of EVs to the US. The main exporter before the COVID-19 pandemic was Vietnam.

Table 3: US’ import from China and China’s export to the US of EVs

| China’s export of EVs to the US | US’ import from China of EVs | |||

| Value (in USD billion) | Share (%) | Value (in USD billion) | Share (%) | |

| 2017 | 0.3 | 16.6 | 0.1 | 23.9 |

| 2018 | 0.7 | 28.1 | 0.4 | 52.5 |

| 2019 | 0.7 | 21.4 | 0.4 | 20.7 |

| 2020 | 1.0 | 20.4 | 0.9 | 33.4 |

| 2021 | 1.8 | 12.6 | 1.0 | 15.3 |

| 2022 | 2.0 | 7.9 | 1.6 | 12.8 |

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations.

Note: There are multiple reasons for discrepancies in exports and imports data so that they don’t always mirror each other. See: https://wits.worldbank.org/wits/wits/witshelp/content/data_retrieval/T/Intro/B2.Imports_Exports_and_Mirror.htm

Table 4: EV export value (in USD million) and share (%)

| China to ASEAN | China to Mexico | China to USA | ASEAN to USA | Mexico to USA | ||||||

| Value | Share | Value | Share | Value | Share | Value | Share | Value | Share | |

| 2017 | 136.7 | 7.0 | 7.8 | 0.4 | 326.0 | 16.6 | 0.1 | 1.1 | 182.4 | 98.3 |

| 2018 | 119.9 | 4.5 | 12.1 | 0.5 | 746.3 | 28.1 | 4.7 | 9.1 | 43.3 | 64.5 |

| 2019 | 202.3 | 6.3 | 21.7 | 0.7 | 685.5 | 21.4 | 31.6 | 24.5 | 20.8 | 65.2 |

| 2020 | 200.0 | 3.9 | 13.8 | 0.3 | 1,033.9 | 20.4 | 43.8 | 28.1 | 24.9 | 36.7 |

| 2021 | 409.5 | 3.0 | 32.0 | 0.2 | 1,750.5 | 12.6 | 74.6 | 33.2 | 1,734.2 | 43.7 |

| 2022 | 1,073.6 | 4.2 | 80.1 | 0.3 | 2,017.4 | 7.9 | 243.9 | 51.2 | 2,341.5 | 54.8 |

| Note: Value in USD million. Share in %. | ||||||||||

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations

Figure 4: Source countries for ASEAN’s import of EVs (%)

Source: World Integrated Trade Solution (WITS, accessed February 2024), authors’ calculations

In short, while the US-China trade in chips shows signs of ‘decoupling’ (reduced trade values), the US-China trade in EVs shows signs of ‘diversifying’ (reduced trade shares) but not ‘decoupling’.

VALUE ADDITION

Looking at trade in total value or volume may not give the complete picture of trade diversion. China might divert its trade to the US through intermediary countries to avoid sanctions or higher tariffs placed on goods coming directly out of China and exports coming out these intermediary countries to the US may actually be high in Chinese content.

It is therefore important to also look at trade in value-added (TiVA) data of goods and services, which measure the value added by each country in the production of goods and services that are consumed worldwide (gross production minus the purchased intermediates). We use the OECD TiVA data used in Baldwin (2024) to analyse the changes in ASEAN participation in the global value added:

- ‘Foreign Production Exposure: iMport side (FPEM)’: Share of imported input from a source country out of all industrial inputs (including domestically source inputs) used by a country on a scale of 0 to 100. Industrial inputs extend beyond the manufacturing sector and includes the agriculture and service sectors as well. The higher the index, the more reliant (and exposed) a country is to the source country on the production side.

- ‘Foreign Production Exposure: eXport side (FPEX)’: Share of a country’s manufactured production from the manufacturing sector that is exported to a particular partner on a scale of 0 to 100. The higher the index, the more reliant (and exposed) a country is to the destination country on the sales side.

Data for ASEAN are taken as the average of all ASEAN countries. Instead of looking at reliance of trade in value-added in the chips and EV industries, we look at reliance of trade in value-added in the whole economy. With a lag in the OECD TiVA data (the latest TiVA data is for 2020),[6] we may not be able to see the impacts of the more current policies such as the CHIPS and Science Act and the Inflation Reduction Act. However, we can observe a longer-term trend of trade in value-added, including China’s increasing dominance and ASEAN’s increasing participation in global value added.

The US reliance on China’s industrial inputs skyrocketed since the mid-1990s to decline since 2015, albeit with a slight up-tick in 2022 (Figure 5a). Despite this decline, in 2020, US’ reliance on China’s industrial inputs was still three times higher than China’s reliance on US industrial inputs. On the sales side, China’s reliance on the US was more than 17 times higher than US reliance on China in 1995, but the ratio declined since the early 2000s to two times in 2020 (Figure 5b).

Figure 5a and 5b: US-China reliance on the production side, and US-China reliance on the sales side

Source: OECD TiVA (updated 2023, accessed February 2024), authors’ calculations

How has the participation of ASEAN economies in global value added changed?

China replaced the US as the dominant industrial input source for ASEAN countries in 2003 (Figure 6a). In 1995, ASEAN’s reliance on US industrial inputs was three times ASEAN’s reliance on China inputs. In 2020, ASEAN’s reliance on China’s industrial input was more than five times ASEAN’s reliance on that of the US. Similarly, China replaced the US as the dominant industrial output destination for ASEAN countries in 2011 (Figure 6c). In 1995, ASEAN’s reliance on the US market was more than eight times ASEAN’s reliance on that of China. In 2020, this flipped, with ASEAN’s reliance on China’s market coming close to 1.5 times ASEAN’s reliance on that of the US. Conversely, China’s reliance on ASEAN’s industrial inputs and market is increasing and is higher compared to US reliance on those of ASEAN (Figure 6b and Figure 6d).

Intensification of ASEAN’s reliance on both China’s industrial inputs (production side) and the US market (sales side) since 2016 indicates ASEAN’s growing role as an intermediary region for Chinese goods to the US. This is supported by evidence at the country level with the correlation between Vietnam’s exports to the US and Vietnam’s imports from China doubling from 0.4 in 2020 to more than 0.8 in 2024, where 1 shows perfect correlation (The Economist, 2024).

Source: OECD TiVA (updated 2023, accessed February 2024), authors’ calculations

FOREIGN DIRECT INVESTMENT

General FDI trends

Export-oriented FDI inflow positively correlates with the trade pattern. As the trade war intensifies, trade through intermediary countries and the investment inflow going to these intermediary countries surge, including investment to build new manufacturing factories. International investors have relocated or diversified their production locations away from China and sought other Asian economies as destination for FDI to de-risk their businesses from uncertainties arising from geopolitical tensions, pandemic-induced supply chain disruptions, and rising production costs in some countries while seeking potential gains from the new global value chain and emerging sectors such as chips and EVs.

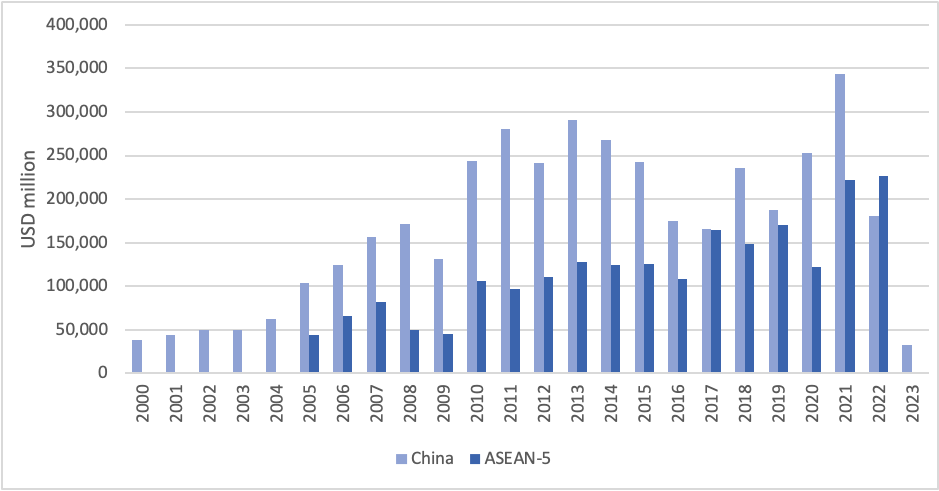

The ASEAN region is a major beneficiary of this FDI relocation (ASEAN and UNCTAD, 2023). FDI inflow to ASEAN-6 (Malaysia, Singapore, Indonesia, Thailand, Vietnam, and the Philippines) reached an all-time high of USD227 billion in 2022 and surpassed the FDI inflow to China (Figure 7). Meanwhile, FDI into China fell to its 30-year low in 2023.

Figure 7: FDI (in USD mn) in China and ASEAN-6

Source: CEIC (accessed February 2024); authors’ calculations.

Note: ASEAN-6 is used instead of ASEAN since other ASEAN countries’ investment data is not up to date.

Reconfiguration of supply chain-related FDI in ASEAN can be categorized into two groups:

- Existing investors expanding their production capacities in the region.

- New investors with/without plant/business presence in China establishing in the region while keeping their presence in China, including Chinese and Taiwanese firms (e.g., the ‘China Plus One’ strategy), or moving their plant and businesses out of China because of the intense US-China conflict.

EVs, EV batteries, electronics and chips, data centres, and the digital economy received robust new and expanded investment in 2022 (ASEAN and UNCTAD, 2023). Manufacturing investment notably scored much stronger growth than in previous years with its share in total FDI in ASEAN rising more than three folds from just nine percent in 2020 to 28 percent in 2022.

FDI by Industry

The electronics and electrical industry accounted for more than 70 percent of new manufacturing investments at USD37 billion, with chips and electronic components alone making up 27 percent of the 70 percent (ASEAN and UNCTAD, 2023), reaching close to USD9.5 billion in 2022, six times the annual average between 2010 and 2019.

Besides chips and electronic components, the ASEAN region also attracted strong investment in EVs and EV battery production as well as charging stations. New investment in batteries rose by 656 percent in 2022 compared to 2021 to USD8.4 billion, accounting for 23 percent of new manufacturing investment (ASEAN and UNCTAD, 2023). Chips, electronic components and battery production combined accounted for half of new manufacturing investment in 2022. FDI in EV-related sectors shot up from USD2.1 billion in 2019 to USD18.1 billion in 2022 (ASEAN and UNCTAD, 2023).

FDI by source and host countries

It is predicted that FDI flows are being increasingly concentrated to countries that are geopolitically aligned with the investor (Ahn et al, 2023). The US, which recently upgraded its bilateral economic relationship with Singapore, Vietnam and Indonesia, was the largest investor in ASEAN with investment reaching USD37 billion in 2022.[7] It was also the largest investor by far in the manufacturing and financial sector. Japan was the third largest investor after intra-ASEAN investment. Japanese FDI in ASEAN was concentrated in the transportation and storage industry, accounted for 88 percent of investment in the industry, reflecting its interest in the automotive industry, including EVs. FDI from China fell by USD1 billion to USD16 billion in 2022, with investment predominantly being in infrastructure projects, EV-related activities and the digital economy.

How ASEAN countries benefit from the reconfiguration of the global supply chain depends on their specialized capabilities (Varas et al, 2021). For example, outsourced chip, assembly and testing (OSAT) firms have been diversifying their global footprints in Southeast Asia such as in Malaysia, Vietnam and the Philippines. Meanwhile, Singapore captured new investment in new chips factories and hosted one of the world’s leading global semiconductor research institutions, A*STAR, whose research goes beyond chip technology.

RESEARCH & DEVELOPMENT

The recent trade and technology war between the US and China has spurred R&D subsidies. The CHIPS and Science Act of 2022 directs USD200 billion of its total USD280 billion spending for scientific R&D and commercialization into chips (Badlam et al, 2022a). Similarly, the Inflation Reduction Act of 2022 increased and expanded tax credits for R&D activities including to jump-start R&D and commercialization of cutting-edge green technology such as EV (Badlam et al, 2022b). In the same year, China upgraded the country’s tax credits for investment in semiconductor R&D from existing chips subsidies worth at least USD150 billion. The R&D subsidies in chips and green technology spill over to other countries including the European Union and Japan. Although most R&D investment is made to unlock financial constraints in the upstream and midstream industries, it usually has a chain synergy effect that catalyses R&D in the downstream industry and the overall innovation ecosystem.

How does the R&D subsidy race affect ASEAN economies? First and foremost, most ASEAN countries do not have the capability (e.g., human capital, physical capital, and regulatory ecosystem) to do cutting-edge R&D. Second, not all ASEAN countries can afford to engage in a subsidy race. Third, technology has become synonymous with geopolitical alignment and trust is a prerequisite to technology transfers. The US as the largest investor in ASEAN is key to bringing new technology to ASEAN as investment often times comes with technology transfers. At the same time, countries with a good reputation in patent and copyright law have an additional advantage in getting R&D investment.

ASEAN economies will not and should not rush into the R&D subsidy race and could instead promote an ASEAN R&D hub, perhaps located in Singapore, as a way to create a production ecosystem in the region.

CONCLUSION

ASEAN’s high trade reliance on China while having the US (by far) as its largest investor and key source of technology transfers puts it in an increasingly precarious situation if US-China supply chain decoupling intensifies. Forcing ASEAN to choose sides – to be in the US or China supply chain system – will be impossible and disruptive, and ASEAN should continue to take the pragmatic approach and reject that option. In the short run, some ASEAN countries are benefiting from the relocation of global supply chains as shown by trade, value addition and FDI data, but the high level of interdependence of global supply chains and the manufacturing hubs in China suggests that these benefits could be more than offset in the long term by the greater disruption to the global supply chains if the US-China tensions continue to escalate.

REFERENCES

Ahn, J., Carton, B., Habib, A., Malacrino, D., Muir, D. and Presbitero, A., 2023. ‘Geoeconomic fragmentation and foreign direct investment’. Chapter 4, IMF World Economic Outlook: A Rocky Recovery. IMF Publication.

The ASEAN Secretariat and United Nations Conference on Trade and Development (ASEAN and UNCTAD). 2023. A Special ASEAN Investment Report 2023. International Investment Trends: Key Issues and Policy Options. Jakarta: ASEAN Secretariat.

Badlam, Justin, S. Clark, S. Gajendragadkar, A. Kumar, S. O’Rourke, and D. Swartz. 2022a. ‘The CHIPS and Science Act: Here’s what’s in it’. McKinsey & Company Publication. Link: https://www.mckinsey.com/industries/public-sector/our-insights/the-chips-and-science-act-heres-whats-in-it#/

Badlam, Justin, J. Cox, A. Kumar, N. Mehta, S. O’Rourke, and J. Silvis. 2022b. ‘The Inflation Reduction Act: Here’s what’s in it’. Link: https://www.mckinsey.com/industries/public-sector/our-insights/the-inflation-reduction-act-heres-whats-in-it

Baldwin, Richard. 2024. ‘China is the World’s Sole Manufacturing Superpower: A Line Sketch of the Rise’. CEPR Publication. Link: https://cepr.org/voxeu/columns/china-worlds-sole-manufacturing-superpower-line-sketch-rise

Bradford, Anu. 2023. Digital Empires: The Global Battle to Regulate Technology. Oxford University Press.

Curran, E., S. Donnan, M. Cousin, N.D. Tu Uyen, Q. Nguyen, M. Martewicz, M. Averbuch, B. Murray, A. Lee, G. Sihombing, and C. Jiao. ‘These Five Countries Are Key Economic ‘Connectors’ in a Fragmenting World’. Businessweek, Bloomberg New Economy.

Dahlman, Abigail, and Mary E. Lovely. 2023. ‘US-led Effort to Diversity Indo-Pacific Supply Chains Away from China Runs Counter to Trends’. Peterson Institute for International Economics (PIIE) Publication. Link: https://www.piie.com/blogs/realtime-economics/us-led-effort-diversify-indo-pacific-supply-chains-away-china-runs-counter

Ebrahimi, Arrian. 2023. ‘China Boosts Semiconductor Subsidies as US Tightens Restrictions’. The Diplomat. Link: https://thediplomat.com/2023/09/china-boosts-semiconductor-subsidies-as-us-tightens-restrictions/

Economic Development Board Singapore (EDB). 2022a. ‘Southeast Asia’s Rising Semiconductor Fortunes’. Link: https://www.edb.gov.sg/en/business-insights/insights/southeast-asia-s-rising-semiconductor-fortunes.html

Economic Development Board Singapore (EDB). 2022b. ‘Diverse Capabilities, Infrastructure Help Drive Chips Industry in Singapore’. Link: https://www.edb.gov.sg/en/business-insights/insights/diverse-capabilities-infrastructure-help-drive-chips-industry-in-singapore.html

Ing, Lili Yan, and Ivana Markus. 2023. ‘ASEAN in the Global Semiconductor Race’. Fulcrum. ISEAS-Yusof Ishak Institute Publication. Link: https://fulcrum.sg/aseanfocus/asean-in-the-global-semiconductor-race/

Li, Cheng, and Xiuye Zhao. 2023. ‘Renewable energy should not be the next semiconductor in US-China competition.’ Brooking Institution Commentary. Link: https://www.brookings.edu/articles/renewable-energy-should-not-be-the-next-semiconductor-in-us-china-competition/

Lin, Liza, and Karen Hao. 2022. ‘American Executives in Limbo at Chinese Chip Companies After US Ban’. Wall Street Journal. Link: https://www.wsj.com/articles/american-executives-in-limbo-at-chinese-chip-companies-after-u-s-ban-11665912757

Miller, Chris. 2022. Chip War. The Fight for the World’s Most Critical Technology. Scribner Publication.

Nguyen-Quoc, Thang. 2023. ‘The Deglobalization Myth: How Asia’s Supply Chains Are Changing’. Hinrich Foundation Publication. Link: https://www.hinrichfoundation.com/research/wp/trade-and-geopolitics/how-asia-supply-chains-are-changing/

Pangestu, Mari Elka. 2023. ‘Critical Minerals: Challenges for Diversification, Climate Change and Development’. Slide Presentation at Peterson Institute for International Economics Webinar, on 27 April 2023. Link: https://www.piie.com/sites/default/files/2023-04/2025-04-27pangestu-ppt.pdf

Ross, Laura. 2020. ‘Inside the iPhone: How Apple Sources from 43 Countries Nearly Seamlessly’. Link: https://www.thomasnet.com/insights/iphone-supply-chain/

Shalal, Andrea, and Karen Freifeld. 2023. ‘US starts process to restrict some investment in key tech in China’. Reuters. Link: https://www.reuters.com/technology/us-starts-process-restrict-some-investment-key-tech-china-2023-08-09/

Siqi, Ji. 2024. ‘US Congress considers new legislation to further restrict investment in Chinese tech sectors’. South China Morning Post. Link: https://www.scmp.com/news/china/article/3250360/us-congress-considers-new-legislation-further-restrict-investment-chinese-tech-sectors

The Economist. 2024. ‘How Trump and Biden have failed to cut ties with China’. The Economist. Link: https://www.economist.com/finance-and-economics/2024/02/27/how-trump-and-biden-have-failed-to-cut-ties-with-china

Varas, Antonio, Raj Varadarajan, Jimmy Goodrich, Falan Yinug. 2021. Strengthening the Global Semiconductor Supply Chain in an Uncertain Era. Boston Consulting Group (BCG) and Semiconductor Industry Association (SIA) Publication. Link: https://www.semiconductors.org/wp-content/uploads/2021/05/BCG-x-SIA-Strengthening-the-Global-Semiconductor-Value-Chain-April-2021_1.pdf

ENDNOTES

For endnotes, please refer to the original pdf document.

| ISEAS Perspective is published electronically by: ISEAS – Yusof Ishak Institute 30 Heng Mui Keng Terrace Singapore 119614 Main Tel: (65) 6778 0955 Main Fax: (65) 6778 1735 Get Involved with ISEAS. Please click here: /support/get-involved-with-iseas/ | ISEAS – Yusof Ishak Institute accepts no responsibility for facts presented and views expressed. Responsibility rests exclusively with the individual author or authors. No part of this publication may be reproduced in any form without permission. © Copyright is held by the author or authors of each article. | Editorial Chairman: Choi Shing Kwok Editorial Advisor: Tan Chin Tiong Editorial Committee: Terence Chong, Cassey Lee, Norshahril Saat, and Hoang Thi Ha Managing Editor: Ooi Kee Beng Editors: William Choong, Lee Poh Onn, Lee Sue-Ann, and Ng Kah Meng Comments are welcome and may be sent to the author(s). |

EXECUTIVE SUMMARY

• ASEAN Economic Community (AEC) building is a long journey. For continued relevance and impact, the AEC must remain dynamic while taking into consideration evolving contexts and emerging opportunities and challenges.

• Notable progress has been made under the two AEC Blueprints (2015 and 2025), particularly in laying down the frameworks for regional economic integration and community building. Nonetheless, gaps remain in implementation, calling for a more streamlined but result-oriented agenda and stronger institutional coordination.